57% Asset Deployment Readiness: Why Indonesia’s Tech Sector is Primed for a New Wave of Capital Allocation

For years, the operating thesis of Indonesia’s digital economy could be distilled into a single imperative: velocity. Fuelled by a period of near-zero interest rates and abundant venture capital liquidity, startups prioritised rapid market expansion as the prevailing norm across the ecosystem. In this environment, corporate governance was often treated as a secondary consideration, not by design but as a reflection of the market conditions and expectations that defined that phase of growth.

As global macroeconomic conditions shifted, the market underwent a pragmatic recalibration. A period of heightened scrutiny around governance standards and reporting practices across the ecosystem contributed to a shift in investor confidence. Private tech funding consolidated to roughly USD355.7m in 2025, per the Indonesia Startup Report 2026 by Foundry Collective, a contraction from its peak earlier in the decade. The contraction, however, is not evidence of retreat. The ecosystem is undergoing a structural transition, and the terms of that transition are being set at the level of governance infrastructure.

The Shift

The company-level picture has already begun to reflect this. Bukalapak recorded a net profit of IDR3.14trn (trillion Rupiah) for 2025, reflecting a sustained shift toward capital discipline. The GoTo Group reported record adjusted EBITDA of IDR2trn in 2025.

Andi Taufan Garuda Putra, Founder and CEO of Amartha, observed that startup success is no longer measured by growth alone, but by the quality of business fundamentals and real impact. “Investors and founders must align on building sustainable businesses with strong governance and a focus on profitability,” he noted.

The capital picture follows the same logic. Data from Indonesia’s Financial Services Authority (OJK) shows that total assets held by Indonesian venture capital companies reached a record IDR27.57trn in 2025, while actual disbursements held at roughly IDR15.97trn. This gap has widened consistently since 2022, when disbursements of IDR17.61trn were roughly in step with total assets, marking the closest point of parity in recent years. The Investment to Fund Asset Ratio has moved from 69.29% in 2018 to 57.94% in 2025. The available capital is there. The conditions required to unlock it have changed.

The forensic picture explains why. PwC’s analysis of portfolio companies identifies a consistent gap between paper compliance and operational reality. A startup may present audited financials and formalised procedures and still carry material risks beneath the surface because misrepresentation, whether by design or by oversight, can work around standard control mechanisms rather than trigger them. In the B2B and fintech sectors, rapid growth has blurred the boundary between lending and supplier credit, producing financing structures where the boundary between debt obligations and equity position becomes difficult to verify from outside the company.

Several patterns recur across these cases: unusually rapid profitability relative to sector peers, consistent negative cash flows alongside reported revenue growth, significant transactions with related parties lacking independent review, and sudden spikes in receivables ratios that point to premature revenue recognition.

Taken together, these signals indicate that complexity is outpacing the infrastructure built to manage it, a condition that data from PwC’s Global Compliance Survey 2025 confirms at scale. Some 85% of organisations report compliance has grown more complex over the past three years, 63% cite disaggregated data as their primary operational challenge, and 56% report poor data quality. Regulatory complexity drives data fragmentation, and fragmented data is where financial misrepresentation goes undetected.

Addressing this, Maman Firmansyah, Director of Supervision for Financing Institutions and Venture Capital Companies at OJK, noted that governance is the first pillar of industry health, and that weak governance at the start makes downstream risks unavoidable. Sacha Winzenried, Director at PwC Indonesia, noted that as the industry develops, embedding robust risk management early protects both portfolio value and market reputation.

Capital deployment velocity is now directly conditional on governance infrastructure maturity. The gap between assets held and capital deployed is where that condition shows up most directly in the data. The demand for rigorous, scalable oversight is the market response.

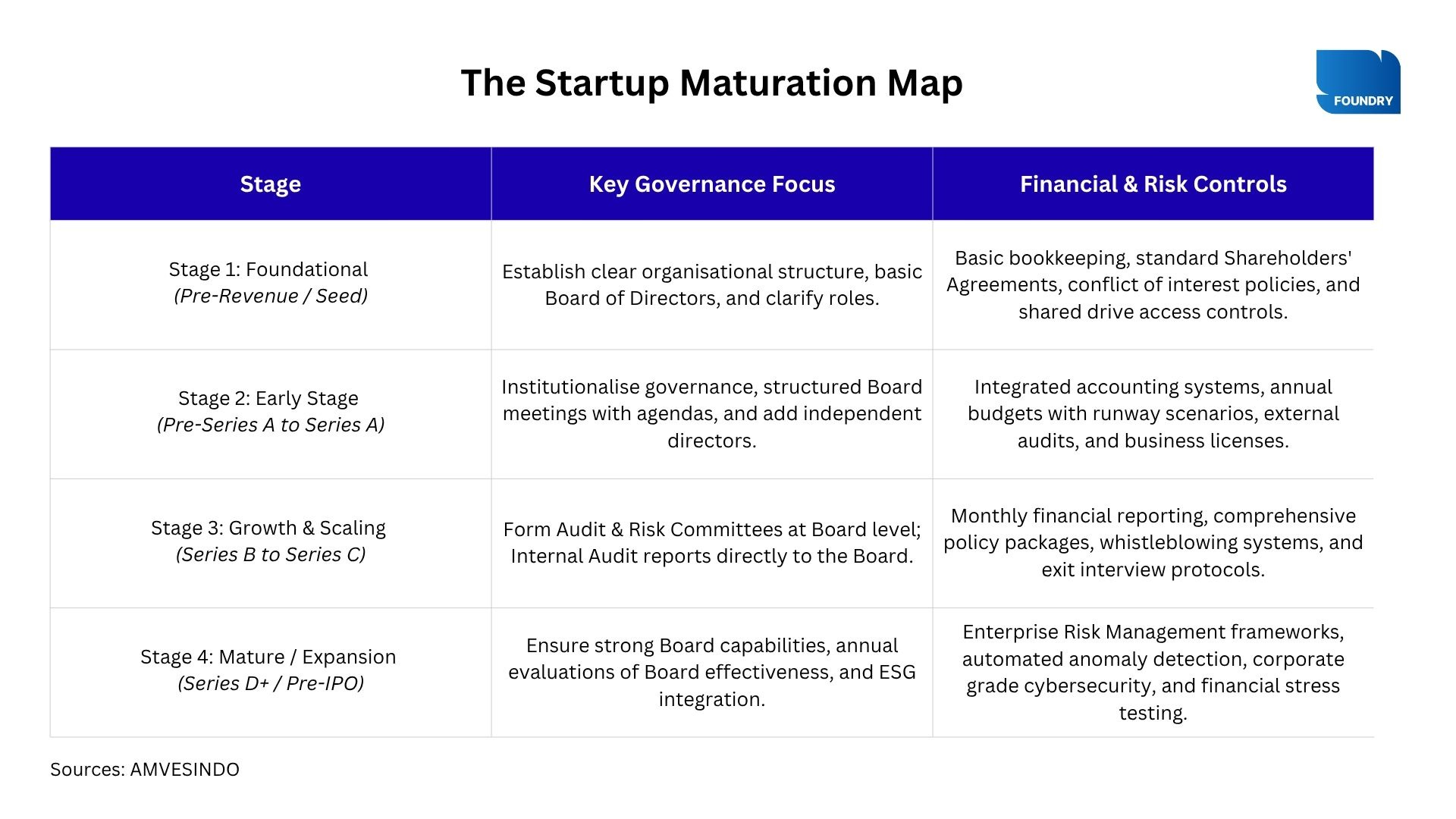

Governance as Infrastructure: The Maturation Map

The demand for stricter oversight creates a practical tension. Early-stage founders commonly view enterprise-grade risk management as a constraint on the speed that early growth requires. Recognising this, the Startup Maturation Map was developed in collaboration with venture capital associations across Southeast Asia, including those from Singapore (SVCA), Malaysia (MVCA), Thailand (TVCA), and Vietnam (VPCA). The framework installs controls incrementally, calibrated to each stage of a company’s development rather than applied as a single mandate.

Eddi Danusaputro, Chairman of AMVESINDO, framed the stakes plainly. In the midst of economic uncertainty, governance and risk management are key not only to business survival but to ensuring the industry can support sustainable innovation.

The Regulatory Layer

The Maturation Map sits within a broader regulatory shift that reinforces its logic from above. POJK 48/2024 on good corporate governance extends its mandate to venture capital companies directly. Under the financial services institution definition in the regulation, venture capital companies are covered as regulated entities. This makes the obligation binding on capital allocators, not only on the companies they back. According to ACFE 2024 global data, anti-fraud policies of the kind now required under POJK 48/2024 are associated with a 50% reduction in median fraud losses among implementing organisations.

Indonesia’s digital economy is growing, in scale, in discipline, and in the institutional architecture required to sustain both. The market fundamentals are intact, the consumer base is expanding, and the venture capital reserves are substantial. What has changed is the condition under which that capital moves. Governance infrastructure is now the variable that determines deployment. Among major emerging digital economies, Indonesia is one of the few where that correlation has been made explicit by both market behaviour and regulatory mandate at the same time. That is the basis on which the next phase of growth will be built.