Social commerce GMV grew 111% in Q1 2026. A strong signal of recovery

Foundry Monthly Recap: March 2026 Edition

As the first quarter of 2026 draws to a close, Indonesia’s technology ecosystem is operating on a different set of terms. The signals are visible across earnings reports, capital flows, and regulatory enforcement and they point in a consistent direction. National GDP growth holds at around 5%, while domestic consumer confidence registered at 125.2 in February, a signal worth tracking in a consumer market of 270 million people.

What this quarter makes clear is not that the ecosystem has stalled. It is that the conditions defining the next cycle are already visible and they are taking shape across multiple layers of the digital economy at the same time.

Public Markets Are Pricing Indonesia's Consumer Tech on a New Standard

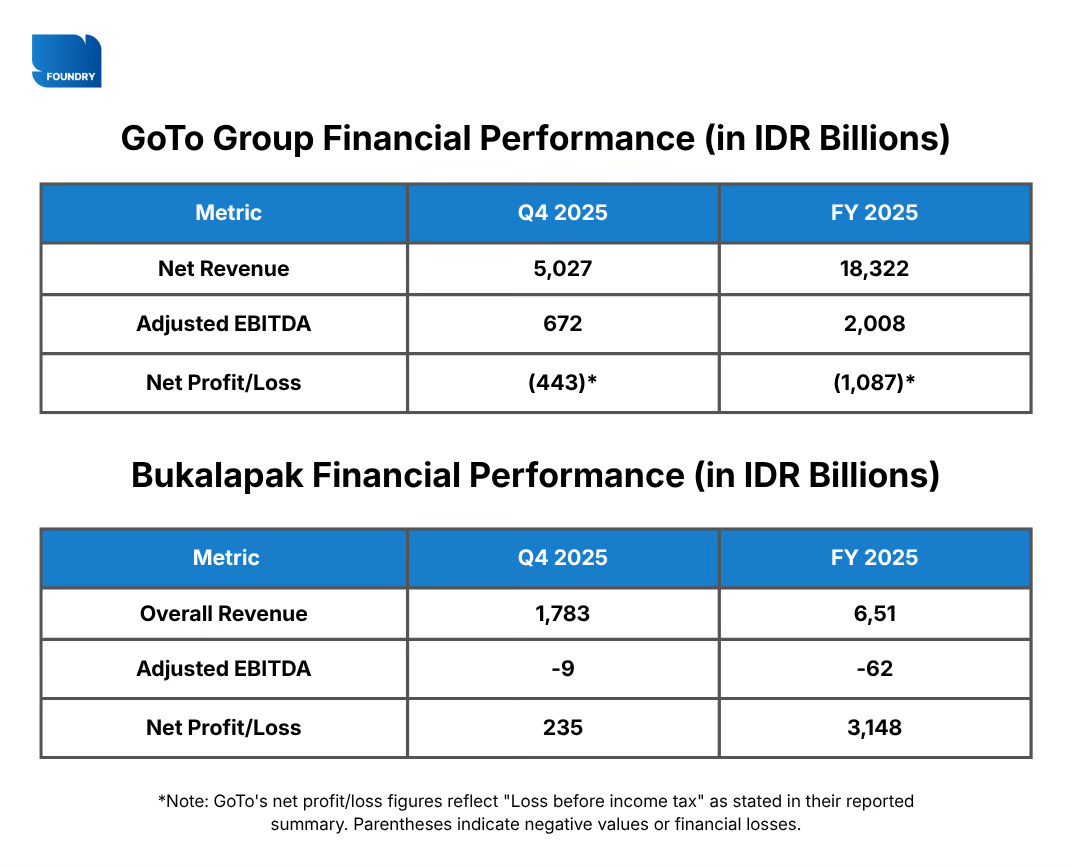

The measure by which Indonesian consumer tech is being valued has shifted — away from theoretical market size and toward actual cash generation. The latest public market data makes this visible. GoTo Group delivered a full-year adjusted EBITDA of IDR2 trillion for 2025, outperforming its prior guidance and projecting up to IDR3.4 trillion for 2026. Bukalapak narrowed its adjusted EBITDA losses to IDR62 billion, operating at effective break-even while holding IDR16.21 trillion in cash.

These are not isolated company achievements but data points in a broader market-level shift where ecosystem integration compounds the effect. When financial products are placed directly inside the daily transaction flows of ride-hailing and e-commerce, customer acquisition costs approach zero. The embedded model earns from users the platform already has rather than paying to find new ones. Bank Jago’s 115% increase in net profit to IDR276 billion was anchored by exactly this structure, through its embedded position within the GoTo ecosystem.

The IPO pipeline is being reshaped accordingly. Institutional capital is allocating toward platforms that monetise existing users rather than those deploying capital to acquire new ones. Traveloka’s reported net profit of USD37.7 million and Kopi Kenangan’s profitability at a USD180 million revenue base reinforce this as a sector-wide condition. Embedded finance and operational discipline are the mechanisms through which scale is being converted into defensible margins.

Healthcare Capital Is Moving Toward the Physical Layer

Post-pandemic capital allocation in Indonesian healthcare has reoriented. Early investment into asset-light telemedicine and health applications has given way to targeted positions in physical secondary care and administrative infrastructure, a reallocation that reflects where the system’s structural gaps sit and where foreign and regional capital sees the more durable opportunity.

The numbers point to where the gaps are. West Java, a province of nearly 52 million people, has a hospital bed density of 0.85 beds per 1,000 people, below international benchmarks. When the physical infrastructure cannot handle the volume, expanding digital access at the front end has limited effect.

Sweef Capital’s strategic investment in Avisena Healthcare Group, a four-hospital network targeting this capacity gap, addresses the referral bottlenecks that persist within the BPJS Kesehatan system at the infrastructural level rather than at the digital interface.

The administrative layer tells a parallel story. TelkomGroup’s divestment of AdMedika to Singapore-based Fullerton Health, in a deal reportedly valued near USD100 million, integrates Indonesia’s largest claims management administrator into a regional network processing over 14 million healthcare transactions annually. The transaction addresses the claims processing architecture at scale, the layer of the system that determines whether digitised healthcare access can function at volume.

What the capital flows in this sector are showing is a market-level recognition: the gap between digital healthcare access and physical healthcare capacity is where the structural opportunity sits. It is the same logic visible across the broader ecosystem with capital moving toward structural depth over surface-level growth. Investment that bridges those two layers, whether through physical bed expansion or administrative consolidation, is where capital is finding defensible ground.

The Fintech Playbook Is Now an Export

Indonesian fintech built its model under pressure, competing for customers in one of Southeast Asia’s most crowded domestic markets, with thin margins and high acquisition costs. The embedded finance structure that emerged from that environment is now generating real returns. And as the domestic credit market matures, the same playbook is being taken abroad.

Domestically, the embedded finance model is generating results. Superbank posted a pre-tax profit of IDR143.3 billion for 2025, a turnaround driven by a 160% increase in net interest income, and moved up to the KBMI 2 classification, reflecting stronger capital reserves and operational scale.

The domestic credit picture is maturing alongside this. Outstanding BNPL balances reached IDR37.44 trillion by late 2025, with banking-based non-performing loan rates at 2.04% and multi-finance at 2.73%. Consumer purchasing power remains under pressure from inflation, and the domestic credit market is approaching the natural limits of its current growth cycle. It is this maturation that explains the sector’s outward movement.

The embedded finance playbook, stress-tested in one of Southeast Asia’s most competitive domestic markets, is now the asset being exported. Kredivo Group’s acquisition of a 100% stake in Timo, Vietnam’s pioneering digital bank, is the clearest expression of this. Backed by USD100 million in recent funding and committing USD15 million in fresh investment over three years, Kredivo is replicating a model that has already demonstrated its viability at home. Vietnam is not a new experiment. It is a proven model entering a new market.

The domestic payment architecture is connected with global rails in parallel. DOKU’s partnership with Ant International extends the reach of Indonesia’s payment infrastructure into the broader Asian cross-border ecosystem, giving local merchants direct access to cross-border transaction flows without requiring new infrastructure built from scratch. As domestic credit conditions mature, the operational models built under that pressure become the basis for regional expansion. Indonesian fintech is transitioning from a recipient of cross-border capital to an exporter of cross-border platforms.

Regulation Is Being Built to Last

The instinct when reading a wave of new regulation is to ask what it is stopping. The more useful question, in Indonesia’s case this quarter, is what it is building.

The measures introduced in Q1 2026 are not a single policy response to a single problem; they are the components of a regulatory architecture being assembled in parallel across different parts of the digital economy.

Government Regulation No. 17 of 2025, which prohibits children under 16 from accessing designated high-risk digital platforms, came into enforcement on March 28, 2026. The regulation places compliance responsibility on the platforms themselves, requiring age-verification mechanisms and default privacy settings. By the enforcement deadline, X and Bigo Live had met the requirements in full. TikTok and Roblox demonstrated partial compliance. Meta and YouTube had not met the government’s standards. The government has established access termination as the enforcement mechanism for continued non-compliance and has initiated technical audits across platforms. Indonesia joins Australia among the jurisdictions that have moved from policy discussion to active enforcement on platform access and age safety.

The capital markets picture follows the same logic. The OJK and IDX are requiring approximately 140 publicly listed companies to meet a new 15% free float threshold within the first year of implementation. The measure is designed to reduce ownership concentration and align Indonesian listings with global index standards including MSCI. The share sales required to meet this threshold are estimated at IDR187 trillion. For companies unable to meet the requirement, the OJK has established a formalised delisting pathway. The policy introduces quantifiable implications for listings where ownership concentration has historically been high.

The enabling side of the regulatory posture is equally deliberate. The appointment of Friderica Widyasari Dewi as the new OJK chairperson signals institutional continuity with an active orientation toward digital innovation. The joint launch of the Digital Innovation Center (PIDI) by the OJK and Bank Indonesia makes this concrete through a supervised regulatory sandbox that allows fintech experimentation, including within digital assets, while maintaining consumer protection standards. Enforcement and enablement are operating in parallel, which is what distinguishes a regulatory architecture from a regulatory constraint.

Taken together, these measures describe a state that is setting the structural conditions of the market rather than responding to outcomes after the fact. Compliance is now a market filter, and the costs of non-compliance, whether for a global platform or a domestically listed company, are becoming quantifiable.

The Shape of the Next Cycle

What Q1 2026 describes is a single compounding movement visible from four different angles. The embedded finance model that drove Bank Jago’s profitability is the same playbook Kredivo is deploying in Vietnam. The capital discipline that brought GoTo to positive EBITDA is the same standard institutional investors are now applying to the IPO pipeline. The regulatory architecture tightening platform compliance and capital market structure at home is raising the floor for every participant in the next cycle.

These are not parallel developments; they are the same market recalibrating around a more durable set of operating conditions. The previous cycle was defined by scale. The next will be defined by whether that scale was built on something real.