Quick Commerce in SEA is Worth USD7.3B. Indonesia's 2.8% Online Grocery Penetration is the Region's Largest Untapped Market.

Dear subscriber,

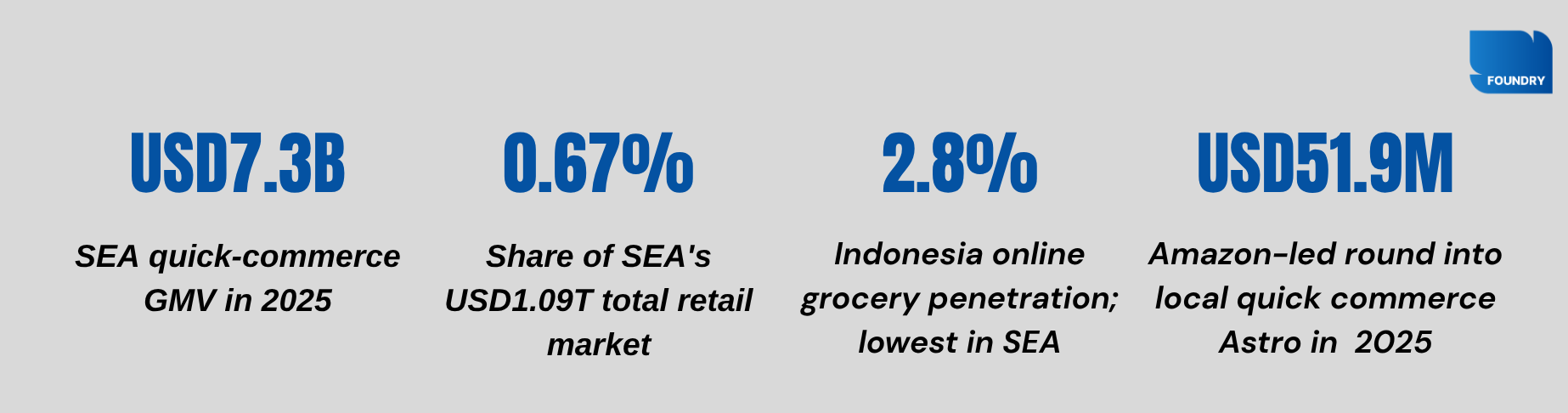

Momentum Works put a number on quick commerce in Southeast Asia for the first time this year: USD7.3 billion in GMV across the region in 2025. That figure is 4.6% of regional e-commerce and 0.67% of total retail. The second number is the structural finding. Quick commerce in SEA is not displacing offline retail the way it did in China or India. It is a fulfillment layer sitting on top of one of the most dense and hyperlocal retail networks in the world. The operators that understood that early built accordingly. The ones that didn’t are gone.

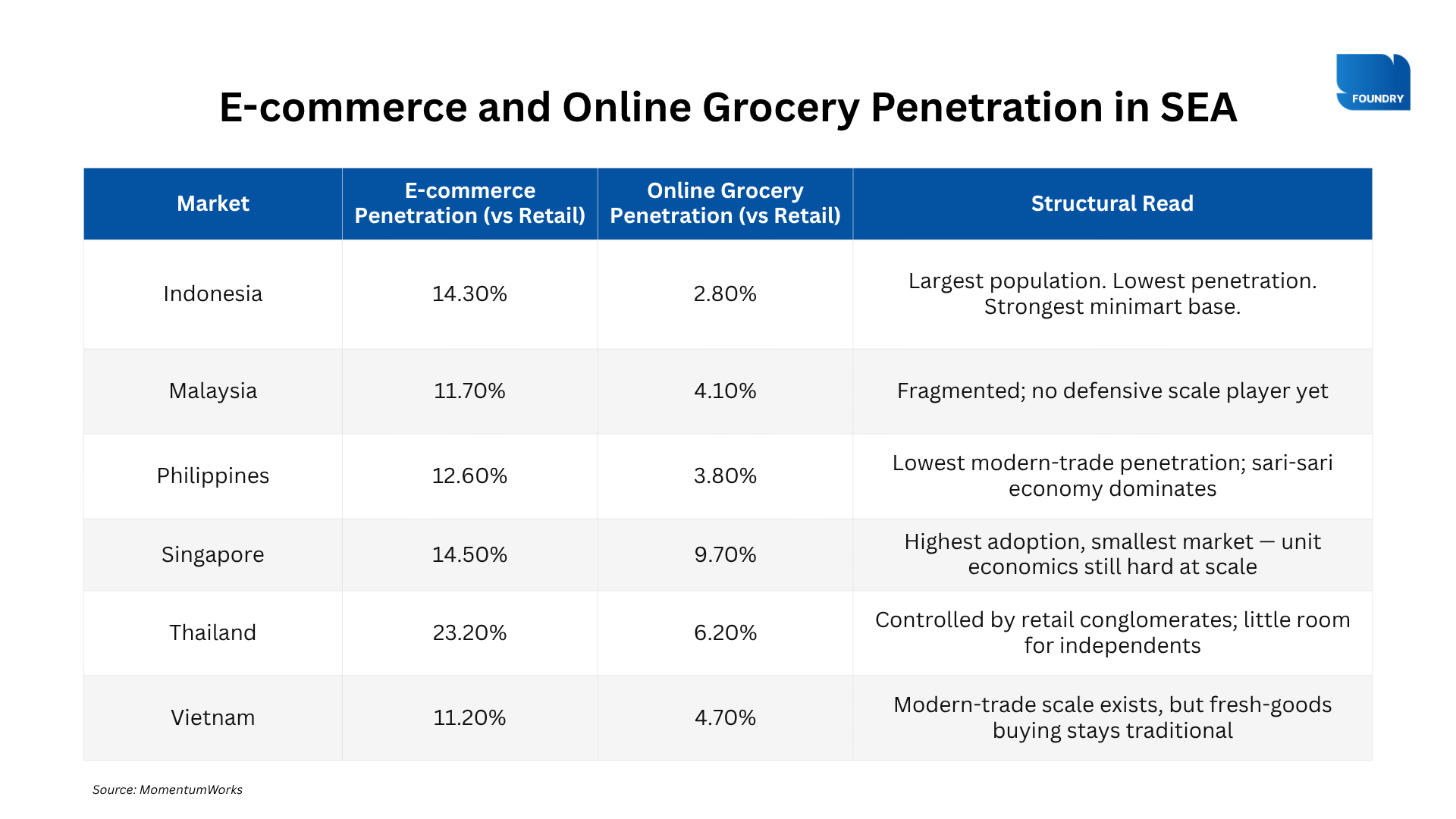

Inside that picture, Indonesia stands out. At 2.8% online grocery penetration, it ranks last in SEA, behind Singapore (9.7%), Thailand (6.2%), Vietnam (4.7%), Malaysia (4.1%), and the Philippines (3.8%). Behind that number: 270 million consumers, the most efficient minimart network in the region, and the most active twelve months the category has seen since 2022. Amazon led a $51.9M round into Astro, Indonesia’s most capitalised quick-commerce operator. Sayurbox and HappyFresh are evaluating a merger. Tokopedia Now is closed.

The reset is finished. The second generation is here.

Stay sharp,

Foundry Collective

Quick Commerce is 0.67% of SEA Retail; and Built to Add, Not Replace

The Momentum Works finding that matters most is also the simplest: quick commerce is 0.67% of total retail and 4.6% of e-commerce across SEA. Unlike China or India, where quick commerce competes directly with brick-and-mortar through displacement, SEA’s offline retail is too dense, too local, and too efficient to be replaced. What works here is the on-demand fulfillment layer that integrates with existing infrastructure.

That single insight separates the survivors from the closures.

Indonesia is the standout because the underweight is structural, not cyclical. Alfamart and Indomaret already operate one of the most efficient hyperlocal retail networks in the world, a duopoly with little incentive to build an independent quick-commerce layer when the offline economics work. That means the addressable opportunity for an on-demand operator is precisely the catchments and categories the minimarts can’t service in 15 minutes or won’t compete in on quality.

Every Indonesian platform that survived 2022–2024 did so by building into one of those two gaps. Every platform that tried to compete head-on with the minimart is gone.

The Local Operator That Built What This Market Rewards

If Astro is the clearest case of an outsider building into the whitespace, Alfamart and Indomaret are the clearest case of incumbents owning it.

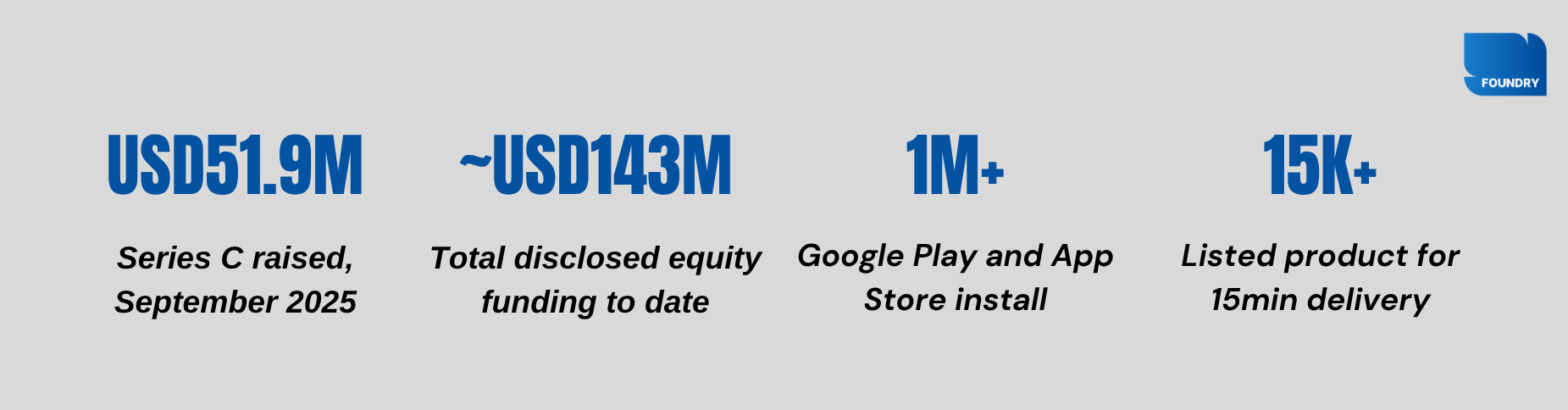

In September 2025, Amazon led a USD51.9 million round into Astro, with participation from Accel, Citius, Endeavor Catalyst, Gemini Investments, Lightspeed, Peak XV, and SBI Ventures. Total raised to date: roughly $143 million. The round closed at a lower valuation than the prior Series B. The frothiness is gone. What is left is a survivor with global backing, a defensible model, and a disciplined cap table.

How Full-Stack Ownership Became Astro’s Competitive Advantage

Astro is the only Indonesian quick-commerce operator that owns the entire stack: sourcing, inventory, dark stores, riders, and last-mile in a country where the easier playbook was to plug into someone else’s. That capital intensity looked like a liability in 2022. Against the Momentum Works thesis, it became the moat.

Hyperlocal dark stores are exactly what the research says wins. Astro operates micro-fulfillment centers across Jakarta, Tangerang, Bekasi, each calibrated for the consumption profile of its catchment. South Jakarta dark stores stock muscat grapes, not standard green ones. That granularity is the layer-on-top-of-retail strategy executed at the SKU level.

Vertical control compresses the cost of every order. Owning sourcing through last-mile means Astro absorbs every margin layer that an asset-light operator pays away. The model is cash-intensive at launch and operationally leveraged at scale, fixed costs are now covered, and every new order in an existing catchment hits a cost base that doesn’t grow proportionally.

Category expansion is the next leg. Momentum Works flags general merchandise and personal-care SKUs as the next extension for SEA quick commerce on top of the grocery base. Astro’s app has cleared 1 million Google Play installs, a base wide enough to monetize the same fulfillment window across multiple basket types without rebuilding the logistics layer.

Amazon doesn’t enter a market on hypothesis. A USD51.9 million lead check, at a moment when Southeast Asian consumer-tech funding sits at a six-year low, is not validation of the category. It is validation of this specific operator. The signal is loudest precisely because the capital environment is tightest.

The Local Minimart Chain is Already Running The Playbook

The operators that understood the SEA quick-commerce thesis earliest did not come from venture-backed startups. They came from the two companies that already owned the infrastructure.

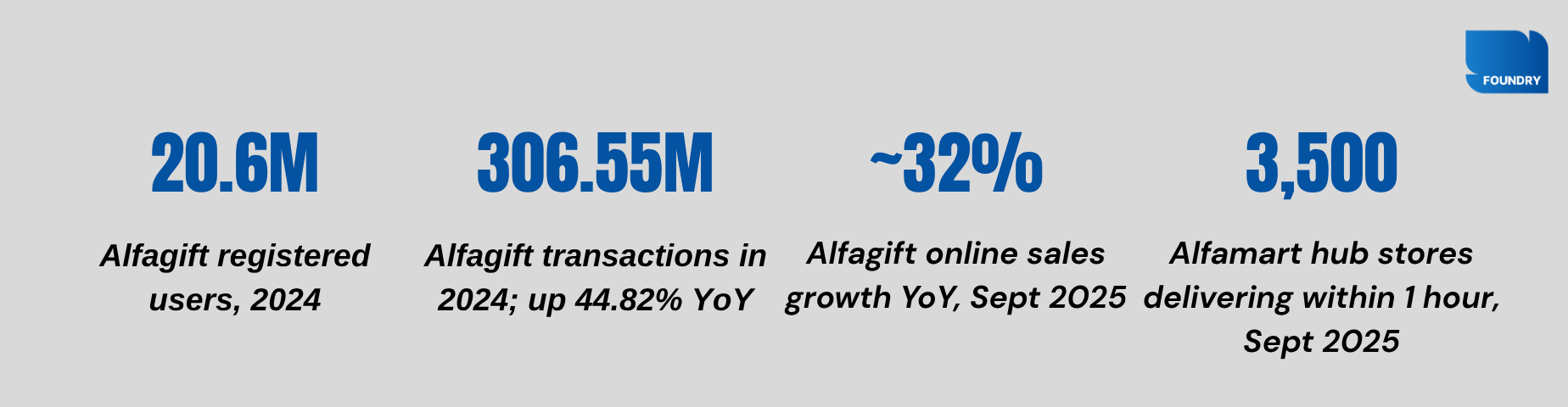

Alfamart and Indomaret together account for approximately 92% of Indonesia’s minimarket sales value. Alfagift recorded 306.55 million transactions in 2024, up 44.82% year-on-year, across 20.6 million registered users — the most-used online grocery application in the country by awareness (62%, Populix 2024). Online contributes 6.6% of AMRT’s consolidated revenue as of the September 2024 disclosure, growing at more than 45% YoY.

The structural reason this works is the same reason standalone operators struggled: Alfamart does not need dark stores. Its SAPA (Siap Antar Pesanan Anda) service converts all 20,925 physical outlets into micro-fulfillment hubs with a 30-minute SLA. Every new store opening is simultaneously a logistics node. Indomaret runs the same logic at even greater scale — 23,441 stores, 46 distribution centers — through Klik Indomaret and its GrabMart partnership, without disclosing digital metrics publicly.

This is the “additive, not disruptive” pattern in its most mature form. The minimarts define the edges of the whitespace. For the operators building inside those gaps, that is a more legible market, not a harder one.

The 2022–2024 Shakeout: Six Closures, Two Survivors, Stronger Unit Economics

Between 2022 and 2024, the operating lineup in Indonesia’s quick-commerce sector got dramatically shorter. Dropezy closed its Jakarta dark stores. Traveloka Mart lasted six months before shutdown. Grab closed its own dark stores and outsourced fulfillment to Trans Retail. HappyFresh exited Malaysia and Thailand, restructured under venture-debt advisers, and wound down most of its Indonesia operations.

On July 16, 2024, GoTo discontinued Tokopedia Now — the quick-commerce arm of the country’s largest e-commerce platform, as part of its post-TikTok-deal business review.

Each closure looks like a setback in isolation. Read together, they look like a market doing what markets do: concentrating capital, attention, and order flow on the operators with the best unit economics. The same pattern played out in India’s quick-commerce shakeout in 2022 and the US grocery-delivery shakeout in 2016.

In every case, the survivors emerged with stronger pricing power, better operating discipline, and disproportionate access to incremental capital.

Why the First Gen Online Grocery Model Hit a Ceiling and What Replaced It. Online grocery platforms built on partner supermarkets worked when capital was cheap and promotional spend could subsidise growth. When the cost of capital rose, that bridge closed. What survived was the operators who had already gone vertical and built their own supply chains before the cycle turned.

Quick commerce is not a feature. Grab and Tokopedia both ran quick commerce as a product inside a larger portfolio — shared logistics, centralised costs, no dedicated focus. When profitability targets tightened, it was the easiest line to cut. The order flow didn’t disappear. It moved to the operators who had built the right infrastructure from the start.

The Operators That Survived Didn’t Try to Do Everything. Astro built exclusively around dark stores and fast delivery. Kept its scope narrow and its operations deep. When broader platforms ran out of runway, Astro had already built something no one else could replicate quickly. That’s why it’s still here.

When the noisy operators leave a market, the quiet ones don’t have to fight as hard for the same demand. That’s the underappreciated dynamic of every shakeout, and it’s the one currently playing out in Indonesia’s quick-commerce order flow.

The Sayurbox–Happyfresh Potential Merger

The most consequential potential move in Indonesian quick commerce right now is not a funding round. It’s a merger that hasn’t been announced. On May 20, 2026, DealStreetAsia reported that Sayurbox is evaluating a strategic combination with HappyFresh, coinciding with a leadership shakeup inside Sayurbox. The two operators are the most enduring e-grocery names left in Indonesia after the 2022–2024 cleanup.

The deal is exploratory, not announced, but the strategic logic is loud, and the investor alignment is the most interesting part of it.

Three things make this more than a standard distressed roll-up:

It would bridge two opposing super-app ecosystems. HappyFresh is backed by Grab. Sayurbox has historically been associated with GoTo-owned Tokopedia. A merger would put the two largest digital-economy ecosystems in Indonesia on the same side of a single e-grocery cap table, a level of cross-ecosystem cooperation with no precedent in this market. That alone changes how the next round of capital prices the combined entity.

Sayurbox has already rebuilt the model the merger would scale. Post-pandemic, Sayurbox shifted to a hybrid B2C/B2B structure and expanded into physical retail through Sayurbox Supermarket, the operating model Momentum Works describes as winning. HappyFresh’s remaining assets: customer base, store partnerships, brand recognition, plug directly into that model rather than replicating it.

Both companies have survived their corrections. HappyFresh restructured after halting regional operations. Sayurbox navigated multiple workforce reductions, focused on profitability. Both are consolidating from operational refinement; and that is precisely what makes this potential M&A consequential beyond its own cap table.

Why Indonesia is The Highest-Potential Node in SEA Quick Commerce

Indonesia’s quick-commerce market is structurally underweight. That is the bullish read, not the bearish one. Every percentage point the grocery-online line moves toward Singapore’s 9.7% adds billions of incremental GMV to whichever operator catches the flow. The first generation tried to force that conversion through promotional spend. They failed. The second generation will earn it through density, category depth, and consolidation, with less competition than at any point in the last four years.

These results are landing in a tighter capital environment, which is precisely why they matter. Southeast Asian consumer-tech funding hit a six-year low in H1 2025. Astro’s down-round Series C is consistent with that. So is the fact that it still got led by Amazon. Discipline is now the price of entry, and the operators that built their unit economics before the cycle peaked are the ones converting that discipline into incremental capital.

Momentum Works named the market: USD7.3B in SEA, 0.67% of total retail, additive to offline rather than disruptive. Indonesia is the largest, most underweight, and most strategically interesting node in that map.

The 2022 cycle proved that quick commerce in Indonesia is not a horizontal e-grocery business. The 2024 cycle proved it is not a super-app side project. The 2025–2026 cycle is proving what it actually is: the hyperlocal, vertically-integrated, category-specific layer sitting on top of one of the most efficient offline retail networks in the world.

The next leg of penetration growth won’t come from the top of the market alone. Category-specific players are quietly building into the gaps the duopoly and dark-store operators don’t prioritise. KedaiMart (part of Kreasi Pangan Indonesia), a Jabodetabek-focused online grocery with ~13,000 SKUs and presence across Shopee, Tokopedia, and Lazada, is one example of an emerging cohort targeting everyday household staples without attempting to replicate the minimart network. Their B2C scale is still early, but collectively, players like these expand the addressable base. If even a portion find durable unit economics, Indonesia’s 2.8% grocery-online penetration moves faster than the structural story alone would suggest.

Astro’s $143M cap table and Amazon’s lead check have already answered the category question. The next decade of Indonesian quick commerce will be built by two or three operators competing on density, not twenty competing on burn.

Indonesia’s quick-commerce market is not recovering. It is resetting: at a higher floor, with fewer operators, and with the most patient capital it has ever attracted.