Pluang Doubled Revenue, FLOQ Hit 1.8M Users. Both Just Raised From Global Capital.

Two licensed operators raised capital in Q2 2026. This edition covers the rounds, the market underneath them, and the regulatory architecture that made both possible.

Dear subscriber,

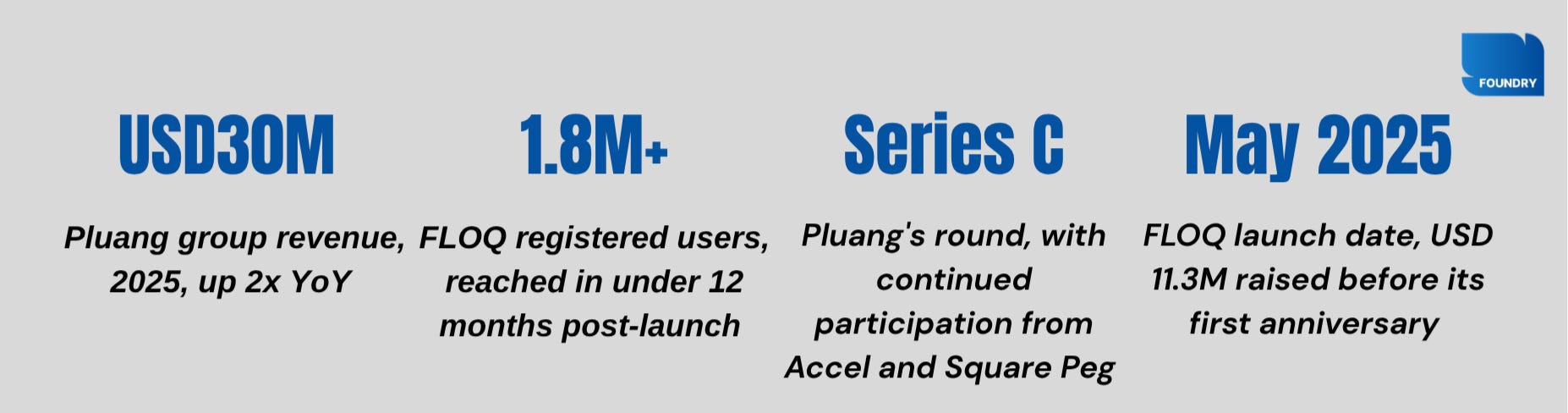

In Q2 2026, two licensed Indonesian digital asset operators closed funding rounds within weeks of each other. Pluang raised a Series C of USD 10 million, led by MUFG Innovation Partners, entering the fundraise from a position of operational profitability and USD 30 million in group revenue — more than double the prior year. FLOQ secured USD 11.3 million from Ascent HFX Group and MD Capital, less than twelve months after launching and after crossing 1.8 million registered users.

Neither round looks like the defensive capital of 2022, when crypto fundraising meant distressed terms and survival positioning. Both operators rose from strength.

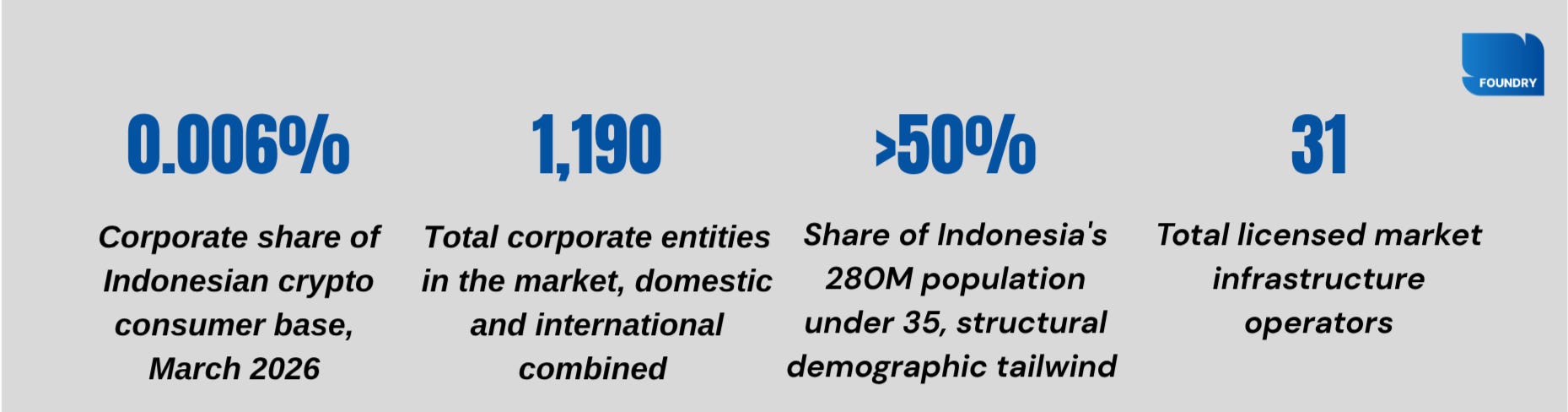

Of the 21 million registered consumers in this market, fewer than 1,200 are corporate entities. That gap is what both rounds are building into.

Stay sharp,

Foundry Collective

Pluang's Series C and FLOQ's Debut Round: Two Positions on the Stack, One Signal

Pluang (PT Bumi Santosa Cemerlang) closed its Series C alongside the official launch of Indonesian equities trading inside its app — a move the company had been building toward since its 2023 acquisition of PT Nilai Inti Sekuritas. MUFG Innovation Partners led the round, with Accel and Square Peg continuing their participation. Co-founder Claudia Kolonas framed the new capital as a reserve for potential acquisitions and international expansion. Pluang manages multiple assets, from Indonesian stocks, US stocks, gold, mutual funds, to crypto.

FLOQ (PT Kripto Maksima Koin) secured USD 11.3 million from private and institutional investors, including Ascent HFX Group and MD Capital. The company launched in May 2025 and surpassed 1.8 million registered users in under a year — a pace that places it among the faster-growing operators in the licensed field. FLOQ operates as one of nine licensed digital asset traders that are members of CFX, the country’s primary digital asset exchange. The capital will be deployed toward technology infrastructure, cybersecurity, product capabilities, compliance, and governance.

Two different operators, two different positions on the stack; one multi-asset wealth platform expanding into equities, one pure-play crypto exchange building out compliance infrastructure; both raising in the same quarter from credible backers, from a position of strength.

21 Million Users, IDR482T in 2025 Volume, and a User Base That Grew

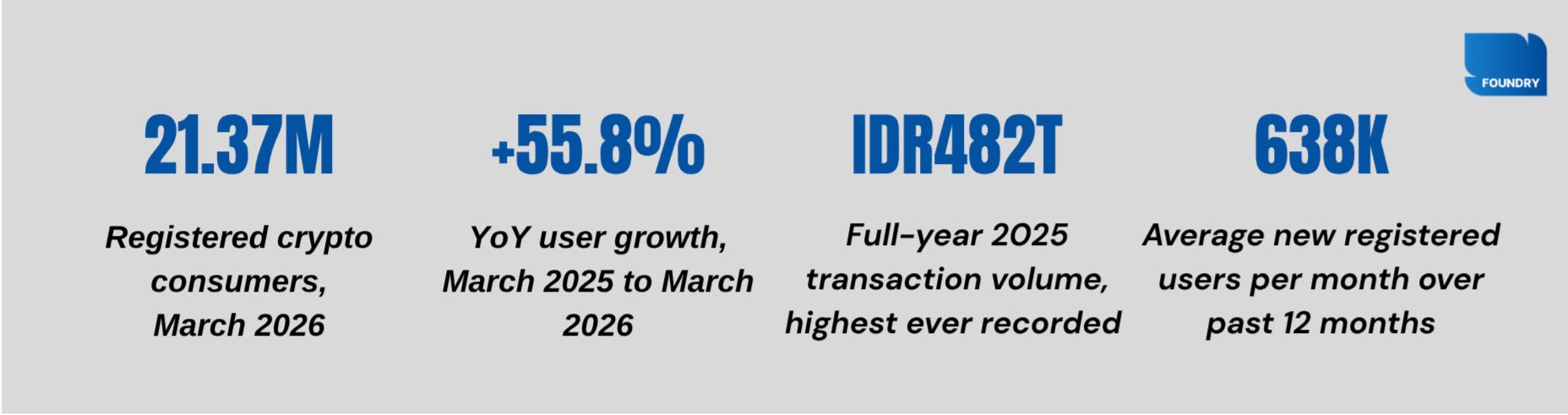

User growth is accelerating, not plateauing. Registered crypto consumers in Indonesia reached 21.37 million as of March 2026, up 55.8% from 13.71 million a year earlier — approximately 638,000 new registered users every month through a twelve-month window that included both a bull cycle and a market correction. The growth did not pause when prices fell.

For context: 21 million crypto investors now exceeds the total stock investor base on the Indonesia Stock Exchange. This is a market where crypto entered the mainstream before equities did for a significant portion of the population. Indonesian user growth held at +48% even through the 2022 bear market, when global growth slowed to +7%.

Volume peaked at IDR 52.50 trillion in July 2025 before normalising through Q4. Q1 2026 contracted 35.4% from Q1 2025, tracking global risk-off sentiment driven by Fed rate uncertainty and US equity volatility — not a structural deterioration of Indonesian demand. User growth continued through the same period. The divergence between rising adoption and falling volume is the classic mid-cycle consolidation pattern: accounts accumulate, activity waits for the next leg.

Four Licensed Layers, One Completed Regulatory Handover: The Infrastructure Is in Place

On January 10, 2025, OJK completed its formal supervisory takeover from Bappebti, replacing a commodity-derivative regulatory regime with a capital-markets-style framework. The difference is structural: Bappebti regulated crypto as a commodity. OJK regulates it as a financial asset, under the same supervisory authority as banks, insurers, and capital market participants.

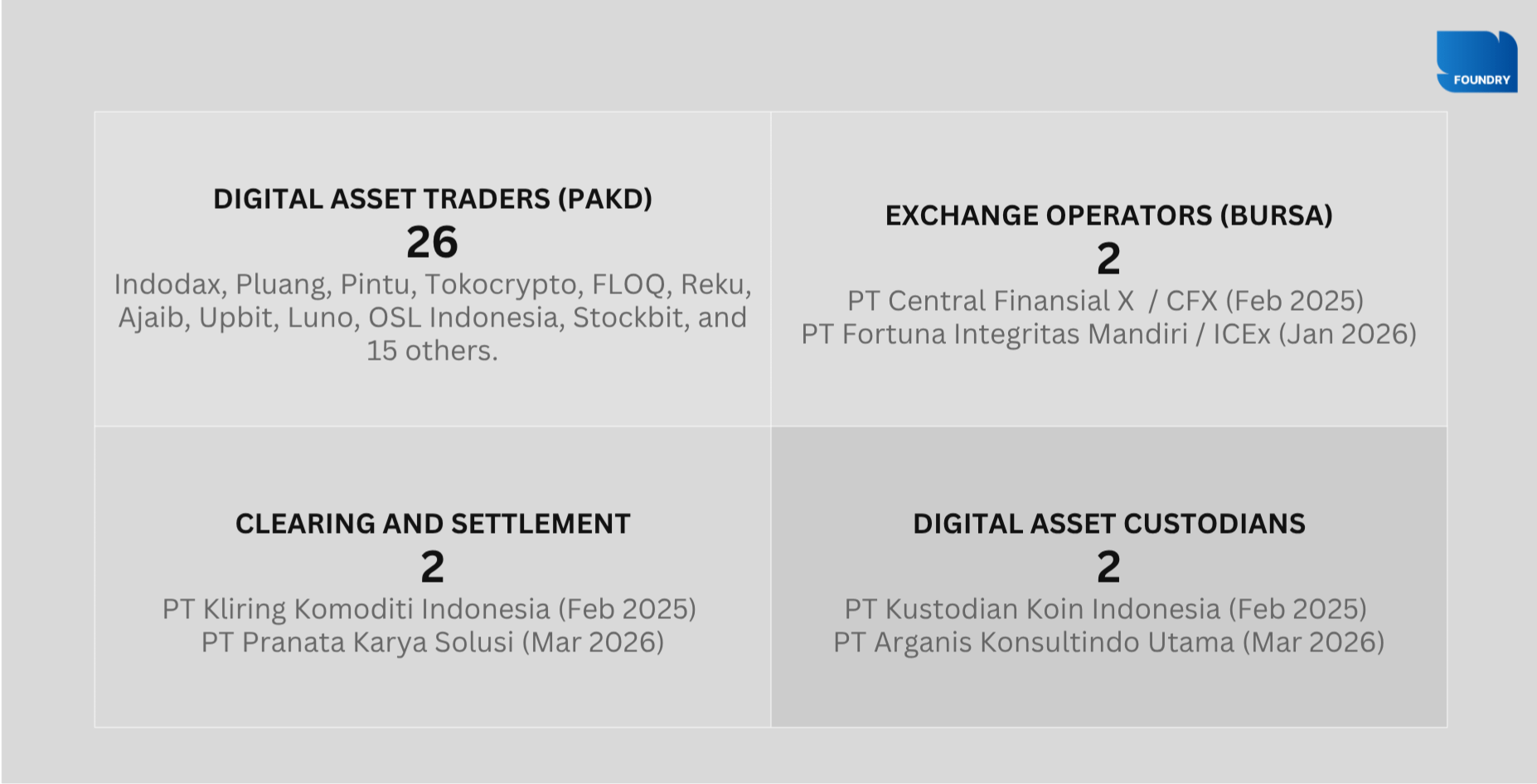

The framework separates market participants into four licensed categories — digital asset traders (26 licensed), exchange operators (2), clearing and settlement institutions (2), and digital asset custodians (2) — mirroring the architecture of a conventional securities market. The four-layer structure was fully in place by March 2026. The enforcement backstop is equally serious: UU P2SK establishes criminal penalties for unlicensed operations — five to ten years imprisonment and fines up to IDR 1 trillion.

The regulatory infrastructure that would allow institutional participation is now in place. The framework has arrived.

As of March 2026, 26 digital asset traders (PAKD) hold active OJK licences, alongside 2 exchange operators, 2 clearing and settlement institutions, and 2 digital asset custodians — 32 licensed entities in total. On the asset side, Bappebti Regulation No. 1 of 2025 (issued January 9, 2025, the last major act under Bappebti’s supervisory authority before the OJK handover) established the tradeable asset universe: 545 assets in the evaluated list (List A) and 851 assets in the candidate list (List B), giving licensed PAKDs a combined tradeable universe of 1,396 legally approved digital assets.

List A assets have passed the full Bappebti suitability assessment; List B assets have been proposed for addition and are under evaluation. Together, they define the scope of what can legally be bought and sold on Indonesian exchanges — a significantly broader universe than most regional comparators and one that includes both blue-chip assets (Bitcoin, Ethereum, Solana) and long-tail tokens spanning DeFi, GameFi, infrastructure, and fan tokens.

The Platforms That Built Before the Capital Arrived are the Ones Positioned to Capture What's Next

The single most important number in the OJK dataset is not the transaction volume. It is the 0.006% corporate participation figure. Of the 21.37 million registered crypto consumers in Indonesia, fewer than 1,200 are corporate entities of any kind — domestic or international. Almost no institutional capital has entered.

The infrastructure to support institutional participation — licensed custodians, a clearing layer, derivative instruments under POJK 23/2025, and international accounting alignment via IFRIC guidelines published October 2025 — is either already in place or was licensed within the past six months. The question of when institutional capital enters the Indonesian crypto market is now a function of internal investment policy at regional and global funds, not a function of what the Indonesian regulatory framework offers.

Indonesia currently has 21 million registered crypto consumers against a stock market with 26 million registered investor IDs. The demographic profile — over 50% of the population under 35, high smartphone penetration — points toward those two bases converging. The platforms that built the right infrastructure before this convergence fully materialises are the ones that will capture the next leg of growth.

Product Innovation as Market Signal

The funding rounds are not the only signal. Three product launches from the same period show the same thesis from different positions on the stack.

NOBI Dana Kripto: Indonesia’s First Professionally Managed Crypto Fund.

Nobi’s asset management subsidiary launched Indonesia’s first OJK-sandboxed managed crypto product (Surat OJK No. S-196/IK.01/2025) in June 2025: an index fund allocating across Bitcoin, Ethereum, and Solana with institutional-grade custody. Backtested returns outperform both standalone BTC and leading conventional Indonesian funds since early 2021. The product is the domestic analogue of the ETF wave — institutional-style access, retail-facing wrapper, built inside the OJK regulatory perimeter.

StraitsX (Fazz Financial Group): Stablecoin Settlement Layer.

USD 22.5 million from UQPAY and NTT Docomo (October 2025) to scale regulated stablecoin payment infrastructure across Asia. The round funds three product lines: institutional on/off-ramp API (XUSD integration), cross-border settlement corridors (including PayFazz for Indonesia’s remittance corridor), and a Visa/RedotPay card programme converting Web3 balances to mainstream merchant spend. XUSD and XSGD are live on Coinbase; OKX Pay runs on StraitsX rails. Strategically, this is the settlement layer that sits above the OJK-licensed exchange and custody stack — the piece that moves value between the regulated crypto perimeter and the broader payments system.

MWX: Agentic AI for SMEs, Built on Web3 Rails.

A MediaWave initiative (led by Nanda Ivens, ex-CMO Tokocrypto), MWX is a Solana-based decentralised marketplace delivering enterprise-grade Agentic AI — autonomous agents for marketing, finance, and HR — directly to SMEs via modular APIs, with fiat and MWXT token payment support. Target: 1 million UMKM users and thousands of AI startups across Southeast Asia by 2028. The market signal here is structural: MWX enters the crypto ecosystem from the application layer, not the exchange layer. It is a product that requires functioning Web3 payment infrastructure to exist — which is precisely what the OJK-licensed stack and StraitsX’s settlement rails now provide.

Two licensed operators, one quarter, both raising from strength. This is what a market that has crossed the credibility threshold looks like.

The setup is unambiguous: 21 million retail investors already in the market, a four-layer licensed infrastructure now fully operational, 1,396 legally approved digital assets on exchange, and a 0.006% corporate participation rate that means institutional capital is essentially absent. The runway ahead is not a forecast — it is arithmetic.

Indonesia’s crypto market has done something most emerging markets fail to do: it built the user base first, then built the regulatory architecture around it. The transition from Bappebti commodity rules to OJK financial services law is complete. The licensed infrastructure is in place. The managed products are launching. The settlement rails are scaling. What has not yet arrived is institutional capital — and when it does, it will enter a market that already has 21 million participants, proven operators, and a regulatory framework designed to receive it. The structural compounders are running. The next leg has not started yet.