75% growth in digital transaction financing. A strong signal of systemic consumption power

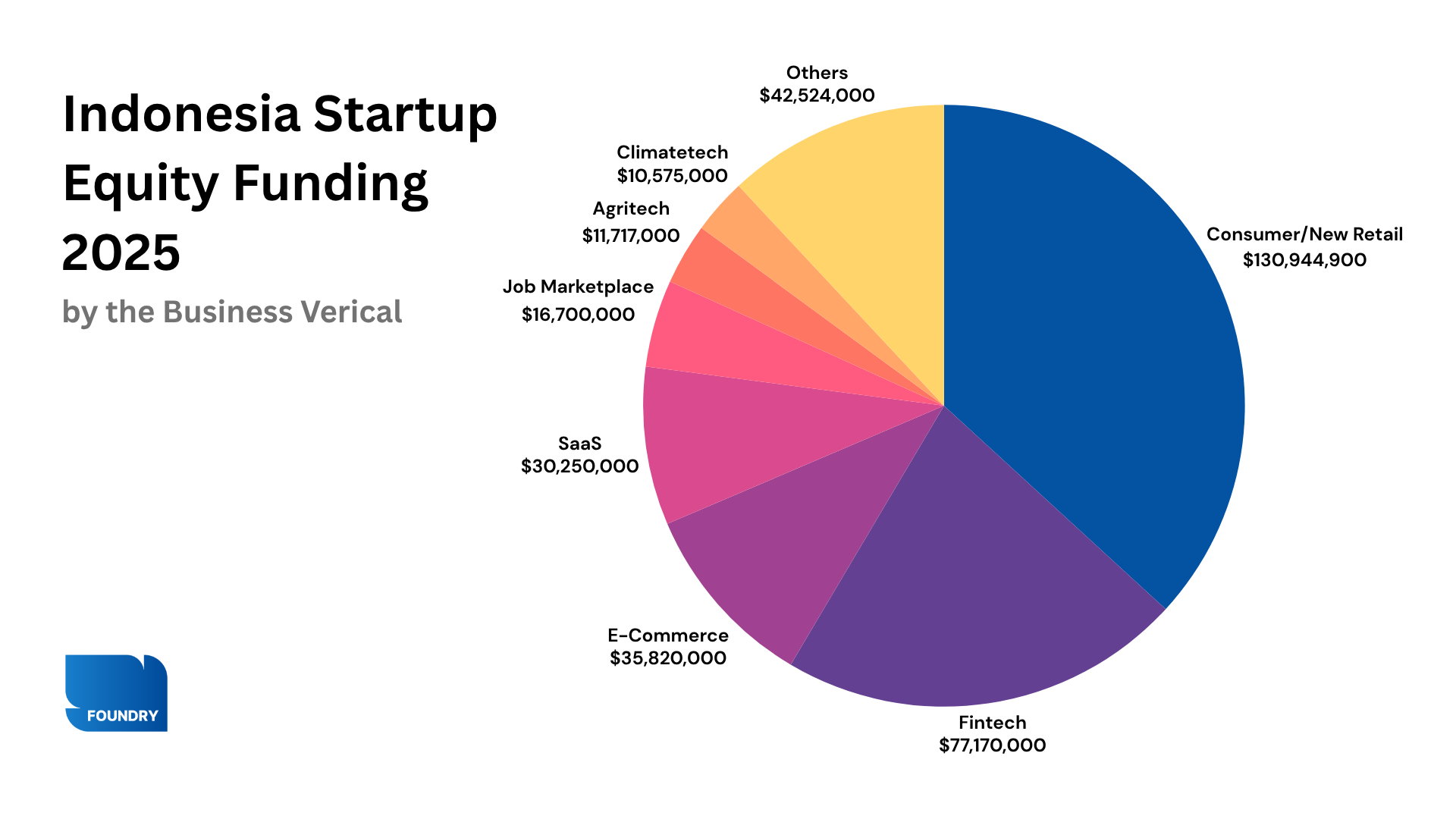

Indonesia’s consumer and new retail sector drew USD 130 million in disclosed funding across fifteen rounds in 2025 — more than double the capital that reached healthtech, the second-ranked category across the Startup Report 2026, which closed eleven deals over the same period. That concentration reflects where the ecosystem’s most experienced allocators are placing their highest-conviction positions.

The consumer sector tracked here covers new retail in its broadest form — D2C brands in F&B, fashion, and beauty; aggregators that acquire and scale consumer labels; and omnichannel retailers building presence across both digital and physical channels. The common thread is the end buyer: these are businesses whose growth is determined by repeat purchase, brand recall, and consumer trust rather than by the infrastructure layer serving them.

Several structural conditions underpin that concentration: an e-commerce distribution layer operating at national scale, a logistics network extending well beyond Java, embedded credit infrastructure converting first-time digital buyers in volume, and an investor cohort with direct experience building category leaders in this market.

The Brand-Building Window is Open

The comparison that surfaces most frequently among early-stage investors is not Southeast Asia at large. It is China’s consumer decade.

Between 2012 and 2018, a sustained expansion of China’s middle-class consumption produced a generation of consumer brands across packaged food, cosmetics, and specialty retail that now hold market positions no subsequent entrant has materially matched. The window to establish durable brand recall lasted roughly six years. The brands that moved within it built recall advantages that compounded into structural market positions, and the category leaders that formed in that period remain the dominant names today.

Joshua Santoso, Investment Director at Alpha JWC Ventures, sees the same pattern forming in Indonesia.

“We believe that Indonesia is approaching that same inflection point in the upcoming years,” he said. “Brand equity and consumer trust take years to build, which is precisely why we invest well ahead of that curve.” He added: “Over the next four to five years, we expect a new wave of category-leading brands to emerge.”

Alpha JWC’s early consumer positions across retail, FMCG, and cloud kitchens each now hold category-leading market share, a result of one consistent operating principle: invest before brand equity is priced in. Once one or two brands hold dominant consumer recall, the businesses that have already earned consumer trust are well positioned to sustain it.

The sectors drawing the most capital are consistent with that logic. Retail and F&B, FMCG, wellness, and specialised healthcare are absorbing the largest share of new allocations, on the basis of returns on invested capital consistent with consumer-category benchmarks in comparable markets, repeat consumption patterns, and demand that tracks middle-class income growth.

The most defensible positions, Santoso noted, are not in empty categories. They are in underserved segments within validated ones, won through execution that competitors cannot quickly match.

Capital efficiency has become the primary filter in early-stage evaluation. A 12-to-18-month payback period is the common baseline, and businesses that perform within or below that range draw the most active allocators.

Santoso points to scale as the reason regional expansion is an option rather than a requirement. Indonesia’s consumer market is comparable in size to Vietnam, Malaysia, and Thailand combined.

A 24-Million-Strong Buyer Base is Building Brand Preferences in Real Time

OJK’s end-of-year data shows how quickly that base of new digital buyers has grown. The credit numbers describe why consumers showed up.

Indonesia closed 2025 with 24.52 million active buy-now-pay-later (BNPL) debtors, a 49.23% increase year-on-year. Total outstanding BNPL financing reached IDR 11.94 trillion by December, up 75.05% from the prior year, according to OJK data. The demographic profile of that growth sits with millennials and Gen Z, two cohorts with high digital activity and a structural preference for flexible credit over traditional banking products.

Those figures describe something broader than a fintech category. They represent a class of buyers who are now transacting regularly through digital channels, building credit histories, and developing brand preferences in real time, at a scale that extends meaningfully beyond traditional credit distribution. Abhijay Sethia, Chief Strategy Officer of Kredivo Group, describes the mechanism:

“Embedded finance provides credit access and flexibility for the consumer, growth for the merchant, and enables the digital economy to compound,” Sethia said. “You simply cannot get mass-market consumers participating in digital commerce at scale without solving for credit and payment flexibility at the point of sale. At the heart of it all sits data, higher transaction volumes feed credit models continuously, creating a compounding flywheel that benefits both merchants and customers.”

Two numbers describe the network’s current footprint. Kredivo’s offline presence now spans more than 50,000 unique store locations across Indonesia, and its collections infrastructure covers more than 90% of the country’s population.

Outside Tier-1 cities, the credit infrastructure is not displacing existing providers — it is creating demand that had no prior equivalent. Serving that market at scale carries specific operational requirements: local marketing, fraud controls, collections discipline, and transaction economics that hold even at lower average basket sizes. The providers building durable positions are those who have localized for them from the outset.

The 24.52 million buyers now transacting through embedded credit are the same cohort in which consumer brand recall is being established for the first time, making the credit infrastructure and the brand-building window two aspects of one opportunity.

A Consumer Sectors Exit Path has Opened at the Growth Stage

Early-stage venture activity is running in parallel with a distinct movement at the growth and buyout end of the market. The result is an identifiable exit path that previously did not exist at scale.

As of April 2026, according to sources familiar with the fundraise, a former senior partner at a major global private equity firm who led several of its largest Indonesian transactions is raising a new mid-market fund, with an indicated target of USD 100 to 150 million and Indonesia’s consumer sector as its primary focus.

This is not an isolated signal. PE firms in the region are reorienting toward essential sectors like healthcare, financial services, and staple consumer goods. Indonesian founders have been building in these categories for years, through a period when a domestic institutional buyer base had not yet formed at scale.

The buyer base is now forming. Consumer sectors have an identifiable institutional buyer at the growth stage — one that did not exist at scale five years ago.

The criteria PE buyers apply at acquisition — audited financials, OJK-compliant structures, documented unit economics, and a clean ownership structure — are becoming the de facto standard for consumer sectors seeking institutional capital at the growth stage. Businesses that build toward them from the outset are the ones that attract competitive bids.

Indonesia’s macro fundamentals support that timing. GDP growth of approximately 5% remains intact, household consumption accounts for more than half of all economic activity, and middle-income demand for staples and essential services continues to expand ahead of discretionary categories.

The variable worth monitoring is rupiah exposure on imported inputs. Businesses with domestic supply chain optionality carry a structural cost advantage that becomes more pronounced as they scale.

The Brands That Scale are Testing Weekly, Not Quarterly

The arrival of institutional capital at the growth stage raises the standard against which consumer sector will be measured. With the infrastructure conditions now in place, the more demanding question sits at the company level, where the distance between opportunity and outcome is measurable in payback periods, repeat purchase rates, and channel discipline.

TJ Tham, Founder and CEO of Tjufoo, a local brand aggregator, returns to the methodological layer that sits above market selection. The most common gap he observes is methodological rather than market-related. Brands that underperform tend to optimize for individual transactions rather than customer segments, and allocate less to brand equity relative to short-term conversion.

The companies that compound, Tham argues, are built on speed of learning rather than speed of scaling. Testing 30 to 40 pieces of content per month, running weekly experiments on product selection, pricing, and messaging: these are the inputs that produce defensible market knowledge. “If you’re not testing at that pace, you’re basically relying on luck,” he noted.

Channel strategy is where the gap is most visible. Marketplaces operate as conversion environments, lower in the purchase funnel, where intent is already formed. Social media and owned channels build brand recognition at the top of the funnel, where intent is being shaped. Treating marketplaces as brand-building surfaces, or expecting social audiences to convert without an intermediate step, produces results that diverge from the channel’s actual function.

Tham offers a specific readiness benchmark for brands that do choose to expand regionally. Those that have cleared Rp 1 trillion in domestic revenue, built presence across both online and physical retail in at minimum Sumatra and Java, and assembled management capable of running independently of the founding team are in a position to consider it.

The Infrastructure is Built. The Constraint has Moved.

Over the past decade, three conditions have come together in Indonesia’s consumer market that rarely align at the same time: a credit infrastructure with national reach, a venture track record that has produced exits in the category, and an institutional buyer base actively positioning at the growth stage. Each took years to form independently. They are now operating in parallel.

That shift changes where the weight of a consumer sector investment actually sits. Structural risk has narrowed considerably, and product decisions and execution judgment now carry most of that weight. The capacity that once went into navigating infrastructure gaps is now available for building the business itself.

The structural conditions of Indonesian market building continue to evolve — talent development in second-tier cities and the time required for category education among them. What has changed is the baseline from which that work now begins.

The inputs for building a category-leading consumer sector in Indonesia are now in place: credit infrastructure reaching most of the population, exit channels that are active and forming, and investors with direct experience in the category. What follows in any market once its structural conditions are established is determined by the quality of what gets built within them. The consumer market that takes shape over the next cycle will reflect the decisions being made now.