26% CAGR: Why the commercial ride-hailing sector is the engine driving Indonesia’s EV growth

For decades, the defining sound of Indonesian cities has been the collective sputter of millions of combustion engines. With over 139 million registered motorcycles, Indonesia is the world’s third-largest market for two-wheelers. Urban transport accounts for up to 80% of greenhouse-gas emissions in the country’s major cities, a direct consequence of that concentration of petrol-powered vehicles.

That concentration of both problem and opportunity in a single vehicle category defines the shape of the transition ahead. For a government that spent roughly USD 45 billion on energy subsidies in 2024 weighted heavily toward fuel imports, the electrification of two-wheelers carries macroeconomic weight alongside environmental intent. Reducing dependence on imported petrol addresses budget exposure to oil price volatility while creating the conditions for domestic industry to develop at scale.

The economic logic has begun to shift. In 2024, Indonesia's battery electric vehicle sales rose 151% year-on-year. Electric two-wheeler sales crossed the 100,000-unit threshold for the first time. By 2025, overall EV sales penetration reached 15%.

The Regional Race and a Distinct Policy Path

The regional context sharpens the picture. Southeast Asia is advancing past legacy automotive markets in EV adoption, and the composition of that growth varies considerably across markets.

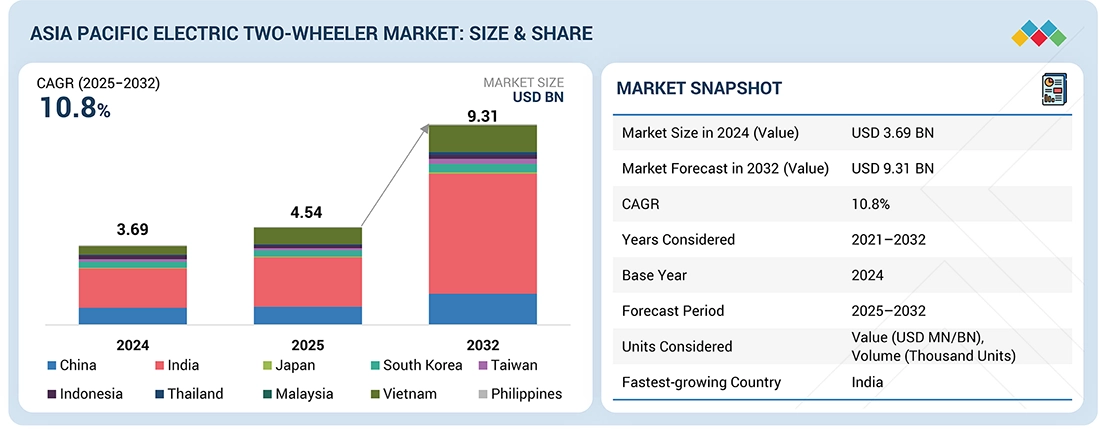

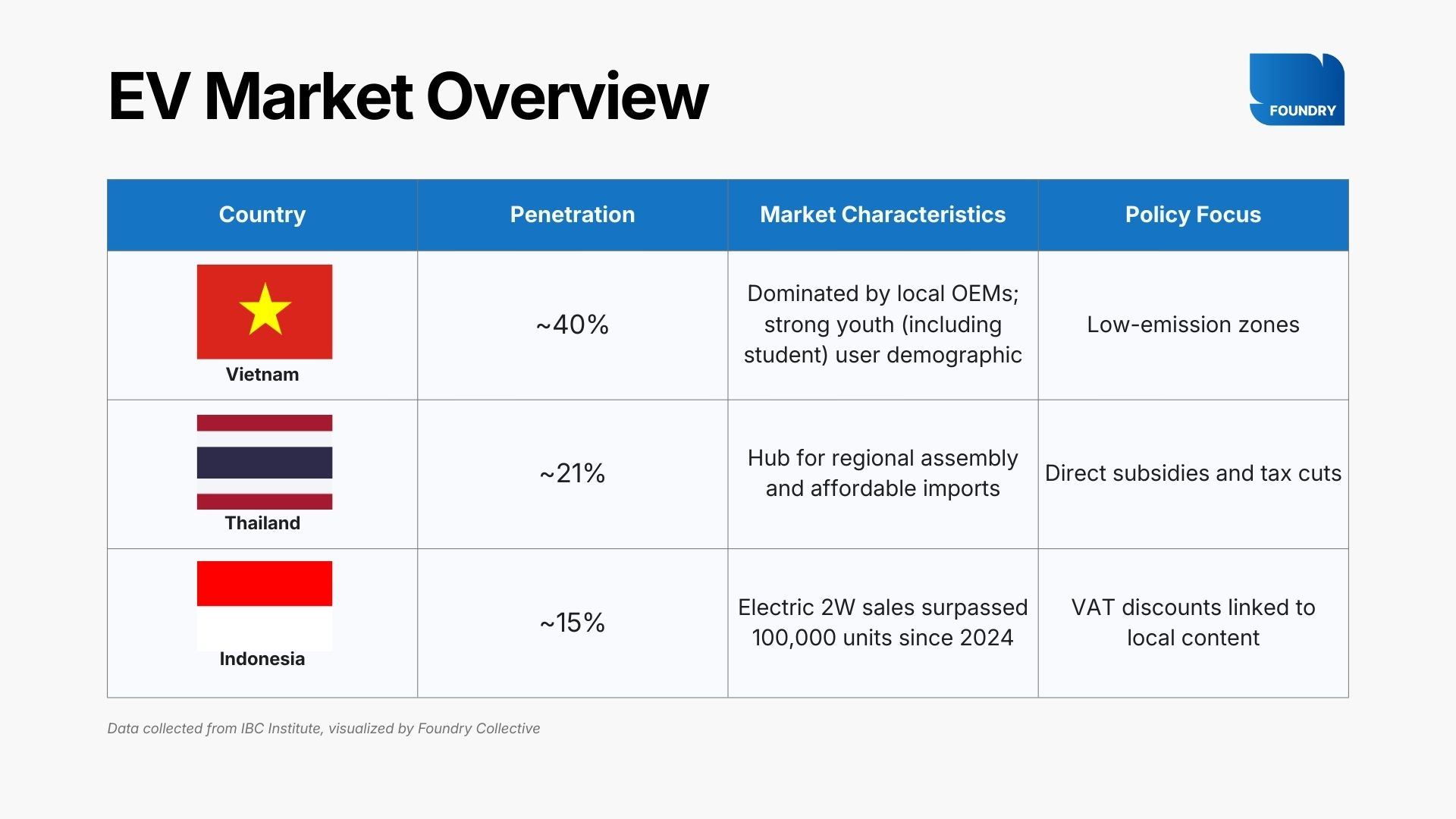

Vietnam leads the region with a 40% EV sales penetration, driven in part by a licensing framework that exempts low-capacity scooters from registration requirements, putting electric mobility within reach of students and first-time riders and anchored by a dominant domestic manufacturer in VinFast. Thailand sits at a 21% EV penetration rate, where import tax reductions and direct subsidies have broadened the affordable segment. Further afield, India's market saw 1.95 million EVs sold in 2024, with 94% of those being two and three-wheelers, supported by the government's USD 197 million manufacturing subsidy programme.

Indonesia has chosen a path that is structurally distinct from its neighbours. As part of a longer-term industrial strategy, the government has transitioned from direct cash subsidies to a value-added tax (VAT) discount tied strictly to local manufacturing. Under this scheme, electric two-wheelers meeting a 40% Domestic Component Level (TKDN) threshold qualify for a 10-percentage-point VAT reduction. This mechanism links adoption growth to industrial capacity, with an eye toward building an industry that outlasts the incentives themselves.

The Upstream-Downstream Divide

The structural opportunity in Indonesia's EV market lies in the distance between its upstream strength and its downstream potential.

Upstream, the country is converting its nickel reserves into industrial capacity: gigawatt-scale facilities are operational, with joint ventures between major automotive and energy storage players, including a USD 1.1bn facility in West Java capable of producing 10GWh of cells annually, anchoring a domestic supply chain. Downstream, public charging infrastructure remains in its early stages, with approximately 4,700 stations in operation as of late 2025 against a government target of 63,000 by 2030. That gap represents the most active frontier for investment and innovation in the market today.

Domestic operators are developing hardware and service models shaped by Indonesia's urban density and logistics requirements. The approach favours modular solutions, battery-swapping networks among them that can scale incrementally alongside the expansion of public charging infrastructure, rather than requiring it as a precondition.

Local Operators, Local Solutions

Much of the active development in Indonesia’s electric two-wheeler market is coming from domestically grounded operators building solutions that require deep local knowledge. Their operational execution illustrates how specific structural issues are being addressed:

Hardware Localization: Maka Motors

The enforcement of the TKDN framework has encouraged a shift from the simple rebadging of foreign kits toward domestic engineering. Maka Motors, founded by ride-hailing veterans, exemplifies this transition. By prioritizing research and development tailored to local infrastructure specifically vehicles designed for the high-humidity and varied road conditions of Indonesian urban centers, the firm has focused on localized R&D to ensure proprietary engineering. This approach suggests that domestic industry can be built on a foundation of specialized hardware rather than imported components.

Decentralized Energy: SWAP Energy

Infrastructure development is also shifting toward decentralized energy networks to bypass grid limitations. SWAP Energy operates a network of over 1,300 battery-swapping stations across 14 provinces, addressing the primary barrier of charging downtime for commercial riders. By utilizing data-driven optimization for station placement and maintenance, the firm has achieved a level of operational efficiency that allows for profitability without a primary reliance on state subsidies. The model indicates that Battery-as-a-Service (BaaS) is a commercially viable alternative to traditional plug-in charging in dense urban environments.

Commercial Fleet Electrification: Dash Electric

The Business-to-Business (B2B) segment is currently the primary catalyst for market growth, driven by the logic of Total Cost of Ownership (TCO). While retail adoption is often slowed by upfront costs, logistics firms are prioritizing the long-term operational savings of electric fleets. Dash Electric facilitates this transition through an EV-as-a-Service platform, allowing businesses to bypass significant capital expenditure by leasing electric delivery vehicles. This model has demonstrated efficacy in the last-mile delivery sector, maintaining high on-time delivery rates while reducing the carbon footprint of national logistics networks.

The Commercial Outlook and Structural Transition

The fiscal trajectory for the sector is defined by high-volume commercial adoption. Indonesia’s electric ride-hailing market is projected to expand from $108 million in 2024 to $690 million by 2032, representing a compound annual growth rate (CAGR) of 26.1%.

This growth is anchored by the commercial fleet sector, where motorcycles account for 63% of operational volume. Commitment from major platform operators to reach full fleet electrification by 2030 has shifted the market from speculative forecasting to a defined procurement pipeline. This scale provides the necessary demand to support localized manufacturing, infrastructure operations, and specialized financing models.

Policy Evolution: From Adoption to Conversion

The state’s ambition to reach 13 million electric two-wheelers by 2030 is being met with a shift in policy focus toward large-scale fleet conversion. Beyond the manufacturing of new units, the Ministry of Energy and Mineral Resources is developing a framework to transition a portion of the nation’s 120 million internal combustion motorcycles to electric powertrains.

The rationale for this conversion programme is dual-pronged: a reduction in localized urban emissions and a strategic reduction in the fiscal burden of national fuel subsidies. While the specific mechanics of the new incentive schemes are currently being finalized for 2026, the transition toward targeted fiscal support suggests a move toward long-term industrial sustainability rather than temporary consumption boosts.

The Macro Perspective

The realization of these targets depends on the continued alignment of upstream capacity and downstream infrastructure. By transitioning from broad consumer subsidies to targeted fiscal incentives and conversion frameworks, Jakarta is attempting to build a domestic industry that is resilient to global market fluctuations. With the integration of the battery supply chain and the emergence of specialized domestic infrastructure models, the structural components for a regional lead in green mobility are increasingly in place.