A 23% Cost Advantage: How Integrating Renewables is Future-Proofing Indonesia’s Export-Oriented Manufacturing

Indonesia’s green transition is often framed as a question of climate ambition. In reality, it is becoming a question of industrial competitiveness. A strategic transition is taking root within the country’s most productive sectors. The country’s power system remains anchored in fossil fuels, but the momentum building around it is not solely driven by environmental aspiration. It is now shaped by the pragmatic logic of industrial economics. Forward-thinking manufacturers are embracing the potential of solar power and green capital to secure a low-carbon future, proving that the nation’s transition is being shaped less by environmental idealism and more by the imperatives of competitiveness and capital discipline.

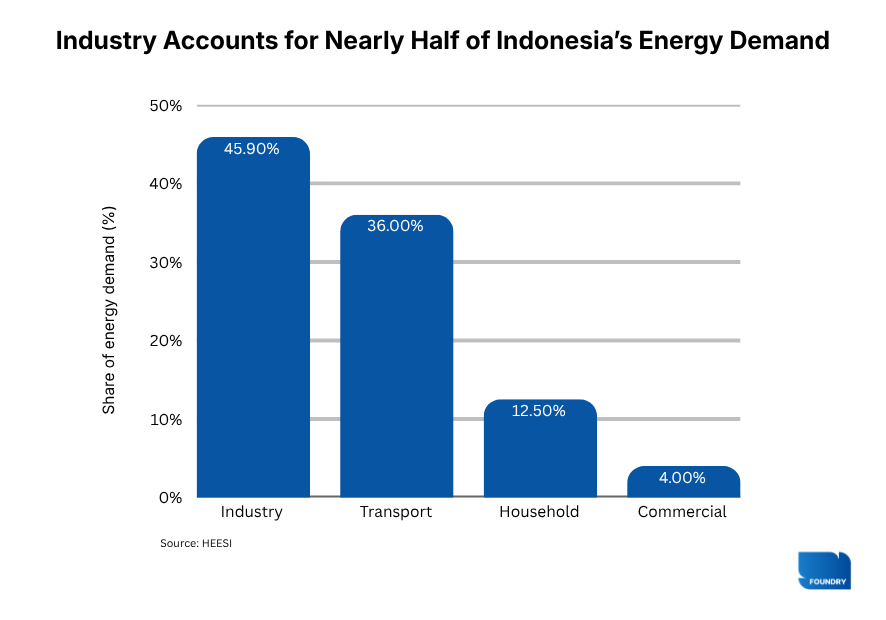

The structural opportunity for decarbonization begins with the scale of Indonesia’s industrial base. Renewables currently account for approximately 14 percent of Indonesia’s primary energy mix. This measure differs from the electricity generation mix but reflects overall energy use across sectors. The concentration of demand within the manufacturing sector provides a clear path for rapid scaling. Official data from the Ministry of Energy and Mineral Resources indicate that industry represents 45.9 percent of total energy demand, nearly four times the share of the residential sector. This disparity means that efficiency gains within industrial estates offer the most immediate and scalable impact for the nation’s energy transition.

According to the Just Energy Transition Partnership (JETP), around 75 percent of Indonesia’s industrial captive power capacity remains coal-based. Another 11 GW of captive projects are in the pipeline, with a majority still expected to rely on coal. The scale of industrial demand makes factories, rather than households, the logical starting point of Indonesia’s energy transition.

When Energy Becomes a Strategic Variable

For export-oriented manufacturers, the cost of carbon is no longer theoretical, it is already determining who remains competitive in global markets. The integration of domestic renewable energy provides a structural pathway toward long-term price certainty and increased energy independence. Currently, Indonesia’s Domestic Market Obligation (DMO) caps coal prices at around US$70 per tonne, significantly lower than global market fluctuations that ranged between US$130–US$140 as of 2024. While this policy stabilizes domestic electricity tariffs in the short term, it also suppresses immediate incentives for renewable adoption. At the same time, it reinforces the strategic rationale for renewables as a long-term hedge against future commodity price volatility should such protections be reduced or removed.

Beyond direct costs, global trade dynamics are now redefining industrial strategy. Export-oriented sectors such as nickel, steel and manufacturing now face mounting external carbon constraints. The European Union’s Carbon Border Adjustment Mechanism (CBAM) and similar regulatory trends effectively price embedded emissions into traded goods. For producers integrated into global supply chains, electricity sources are no longer a domestic policy issue but a competitiveness variable. Carbon intensity now travels with the product.

Financing conditions are evolving in tandem with these trade regulations. International lenders and institutional investors now routinely attach ESG-linked covenants to capital access. International lenders now routinely embed ESG performance conditions into financing structures, with borrowing terms that adjust depending on whether sustainability targets are met or missed. Projects with high carbon exposure may face elevated risk premiums and limited funding options. Renewable energy, then, does double duty: it keeps export doors open and borrowing costs down. This shifts the corporate calculus from a simple comparison of short-term tariffs to a broader focus on long-term balance sheet resilience.

For industrial users, energy stability matters as much as price. While renewable energy requires higher initial capital expenditure, it offers a predictable operating cost structure and greater long-term price stability compared to the commodity cycles associated with fossil fuels.

Commercial viability data supports this direction. A techno-economic study of rooftop photovoltaic systems finds that commercial users achieve annual savings of around 23 percent, compared with roughly 16 percent for households. Solar can cover up to 30 percent of commercial daytime loads, against approximately 22 percent in residential settings. Larger scale and better alignment between operating hours and generation cycles improve the returns further. The evidence points to industrial estates, rather than households, as the primary source of near-term decarbonisation gains. For manufacturers weighing the switch, the numbers make the case on their own terms.

Consider an export-oriented manufacturer in East Java. Its largest European buyer has begun factoring CBAM-related costs into procurement decisions. With EU carbon prices averaged roughly €60–70 per tonne of CO₂ in 2024, based on market estimates and European Commission reporting, the carbon intensity embedded in every product now carries a measurable and growing price tag. For Indonesian exporters without domestic carbon pricing, that liability falls in full on their balance sheet. Its international lender, meanwhile, is attaching ESG-linked covenants to new financing, making carbon exposure a measurable cost of capital. And the domestic coal price cap that has kept electricity relatively inexpensive remains subject to policy revision.

None of these pressures arrives with a fixed deadline. But they are already appearing on the same balance sheet, moving in the same direction, at the same time. For a manufacturer making a ten-year energy decision, that convergence is increasingly part of the calculation. The shift is not being driven by policy alone. It is being priced into the balance sheet.

How The Industry is Adapting

The clearest signal that industrial actors have begun to internalise these pressures comes not from policy announcements, but from procurement decisions. Unilever Indonesia, which operates multiple manufacturing facilities across the country, offers a useful illustration. Facing mounting pressure from its global parent to decarbonise operations across its supply chain, the company moved beyond corporate commitments into concrete infrastructure.

In 2023, it commissioned one of the largest rooftop solar installations in the Jababeka industrial estate in Cikarang, with a combined capacity of 2.5 MWp across two factories. The project is projected to cut CO₂ emissions by around 1,500 tonnes per year. For a company whose buyers and investors scrutinise the carbon intensity of every product, energy sourcing has become a condition of doing business, not a footnote. Unilever’s move is one now being replicated across Indonesia’s export-oriented manufacturing base: that meeting ESG requirements now is cheaper than losing contracts later.

What is changing is not just who is adopting solar, but how. Rather than purchasing assets outright, manufacturers are shifting toward service-based arrangements that remove the capital barrier entirely. Firms such as Xurya offer Power Purchase Agreements and no-down-payment leasing schemes under which factories pay only for electricity generated, while design, installation and maintenance are handled externally. The implication is significant: renewable adoption no longer requires a manufacturer to think like an energy company. It requires only that they think like a buyer.

Beyond rooftops, a parallel shift is under way in how factories source heat and process energy. Agricultural residues such as rice husks, palm waste, and sugarcane bagasse once represented a disposal problem. Manufacturers with access to biomass feedstock now treat them as a fuel hedge. Firms such as Octayne Green have built businesses around this logic, converting waste streams into usable industrial energy. The broader signal is that Indonesia’s industrial energy transition is not converging on a single technology. It is assembling itself from whatever is cheapest and most available. In a country that generates biomass at industrial scale, this calculation increasingly includes materials that were once thrown away.

In practice, this turns renewable energy from a sustainability initiative into a financial strategy, one that stabilises costs, preserves market access and improves access to capital.

From Adoption to Advantage

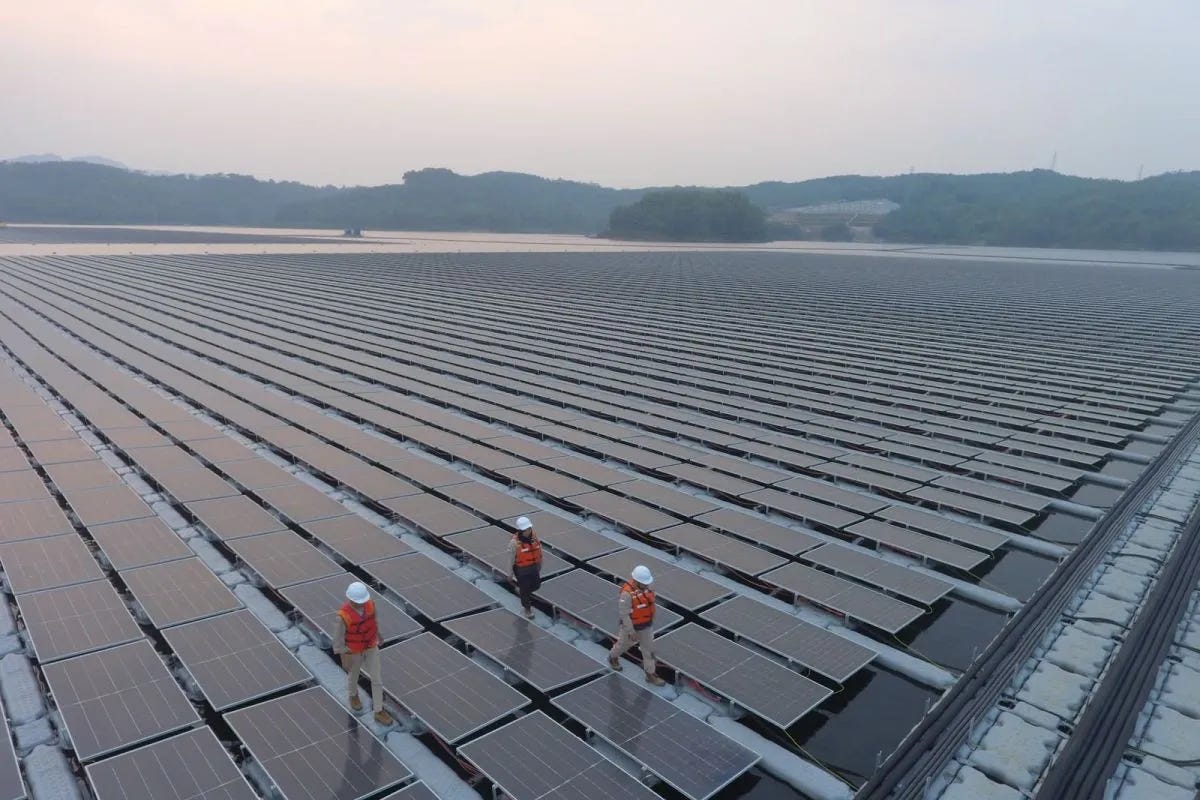

The scale of industrial energy demand is not only reshaping how companies source power, it is also reshaping where renewable infrastructure gets built. The Cirata floating solar plant in West Java is a case in point. With a capacity of 192 MWp, it was designed to deliver utility-scale renewable power without competing for land, as a direct response to the scarcity created by industrial concentration in the region. Less than 5 percent of the reservoir surface is used. The floating design is less a novelty than an engineering response to a constraint. It is an engineering answer to a resource constraint that conventional solar cannot solve on land already spoken for by factories and logistics.

The output bears out the rationale. In its first year of operation, Cirata generated roughly 267 GWh of electricity while avoiding around 214,000 tonnes of CO₂ emissions annually. By integrating solar output with existing hydropower, the plant also improves system stability. Solar supplies daytime load, while hydropower provides balancing capacity. What Cirata demonstrates is not simply that large-scale renewables are technically feasible in Indonesia. It is that industrial-scale demand is now the force reshaping where and how renewable infrastructure gets deployed.

While the industrial momentum is clear, the pace of transition continues to be influenced by the broader regulatory landscape. Indonesia’s coal price cap keeps fossil-based electricity relatively inexpensive. Furthermore, the National Energy Council has proposed revising the 2025 renewable energy target from 23 percent to around 17 to 19 percent. Concurrently, additional captive power projects remain largely coal-based, and decarbonising the captive power sector alone could require around US$31 billion by 2030 and as much as US$92 billion by 2050. This scale of investment also points to where the transition is most likely to take hold first.

Contrary to public discourse that often focuses on the residential sector, data indicates that the industrial sector is the primary engine of change. Industry consumes nearly half of Indonesia’s total energy demand, offering a scale where efficiency gains compound far more rapidly than at the household level. Taken together, these dynamics point to a shift in where and how Indonesia’s energy transition is likely to take shape.

In Indonesia, the energy transition has found its most credible advocate not in climate policy, but in the profit motive. When factories move, they move at scale. In Indonesia, that is where the energy transition will be decided.