A Market in Motion: Indonesia's Startup Ecosystem in 2025

Download Indonesia's Startup Report 2026

Indonesia’s startup ecosystem transitioned into a sophisticated phase of institutional discipline in 2025. While a top-line funding total of USD 355.7 million across 91 deals highlights a leaner capital environment compared to the 2021 peak, it more accurately signals a market successfully recalibrating around the enduring gravity of fundamentals. The Indonesia Startup Report 2026 peers beneath the headline numbers to reveal a landscape of focused innovation and strategic depth that is just beginning to unfold.

Selective Capital, Strong Confidence in Growth-Stage Companies

The composition of 2025’s deal flow reveals more than the total. Later-stage rounds absorbed a disproportionate share of deployed capital, while 67 percent of transactions occurred at pre-seed and seed level, a distribution that, on the surface, looks familiar. What’s changed is what sits behind it: a funnel that now compresses at every subsequent stage, with founders demonstrating product-market fit before capital scales with them. How that progression played out across stages tells a more complete story.

Eight debt transactions appeared in the year’s data. That number is modest; its implications are profound. Debt financing requires cash flow visibility that equity does not, and the subset of companies accessing it in 2025 reached a threshold that speaks to growing financial maturity across select parts of the ecosystem. What that signals about the broader trajectory warrants closer examination.

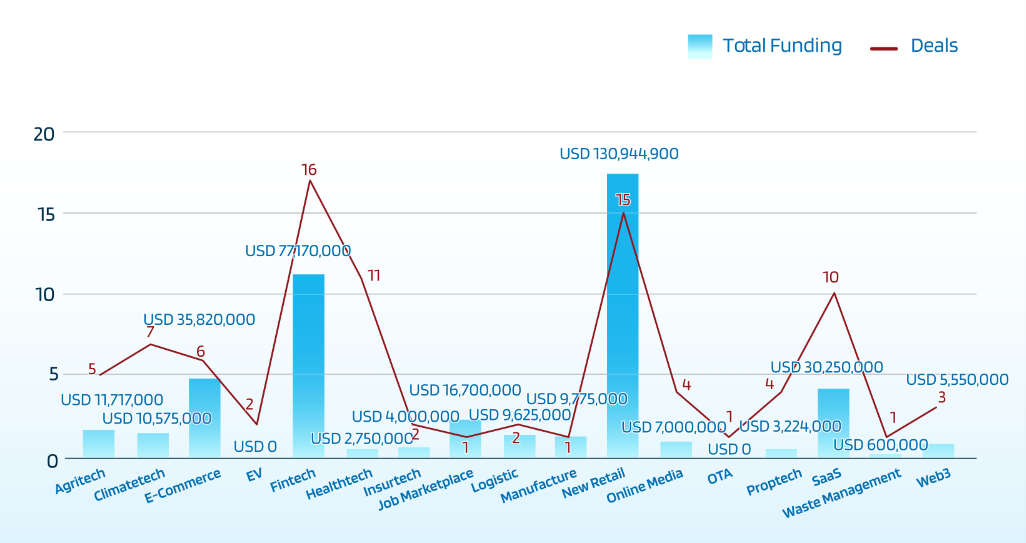

Core Sectors Continue to Attract Capital

Investor concentration in 2025 followed the logic of monetization. New Retail, Fintech, and E-commerce attracted the largest share of capital not because of narrative momentum, but because each demonstrated that Indonesia’s consumer base converts at scale with defensible unit economics. The companies drawing larger checks shared a specific profile: one where margin control is structural rather than dependent on external support. The report maps what this profile looks like in practice and what it implies for how the sector evolves from here.

Fintech’s continued relevance rests on a regulatory shift as much as a commercial one. As frameworks around digital lending, payments, and bank partnerships have become more defined, the risk profile of deployment has moved from exploratory to structural. Indonesia’s financial regulators have tightened licensing requirements and capital thresholds for fintech operators, forcing weaker players out while giving institutional investors greater clarity on compliance and governance expectations. The result is a market where capital increasingly concentrates in platforms able to operate within a regulated framework and demonstrate sustainable lending or payments economics. Capital following clearer rules behaves differently than capital preceding them, and the 2025 flow data reflects that shift in ways the headline figures do not fully capture.

Artificial intelligence registered not as a standalone sector, but as an operational layer embedded across verticals. Applied AI generating leverage across categories with proven demand is a more grounded thesis than AI as a valuation driver alone. How Indonesia’s market is tracking that distinction and where the most durable applications are emerging is one of the more consequential threads of the full report.

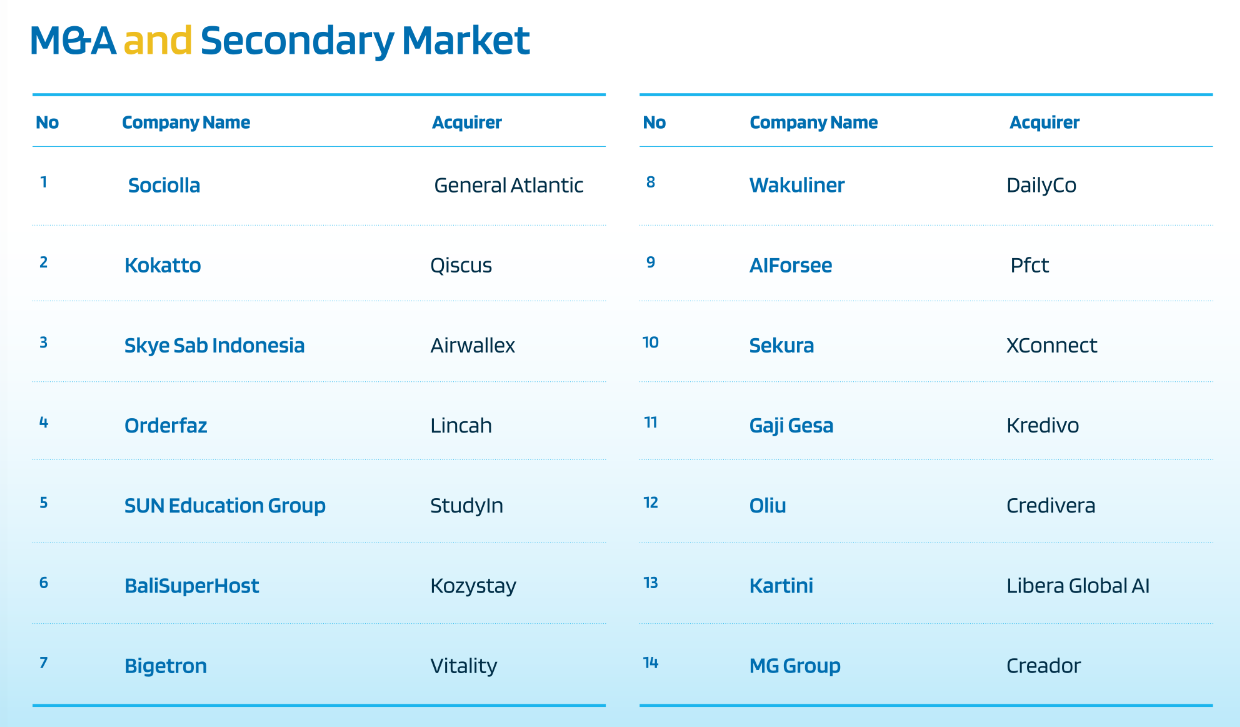

Exit Environment Matures with M&A Leading

The ratio of fourteen M&A transactions to three IPOs is perhaps the year’s most structurally significant data point. It signals the maturation of a functional liquidity pathway that operates alongside public markets, offering a pragmatic alternative to the traditional listing. How active that M&A channel was, which sectors drove it, and what it means for exit planning going forward are questions the aggregate number can only introduce.

Where IPOs did occur, the profile had shifted. Companies listing in 2025 generally demonstrated profitability or credible earnings visibility alongside governance standards closer to regional benchmarks. The quality of listings strengthened a development that reflects the market’s growing emphasis on fundamentals over volume.

A Stronger Foundation for Long-Term Growth

The data reveals that 2025 was not a year of retreat. It was a year of concentration of capital finding fewer, better targets; of exit pathways diversifying; of governance expectations rising to meet institutional standards. The conditions being established now have a bearing on what the next cycle looks like.

Indonesia’s underlying fundamentals remain intact. What is being built on top of them, cycle by cycle, is the institutional layer that determines whether those fundamentals eventually compound or simply persist. The full report provides the space these questions deserve, offering a definitive map of a market in transition.