283% Net Revenue Growth. EBITDA Positive. TipTip Is Building the Economy Behind Indonesia's 17 Million Creators.

TipTip just closed its first EBITDA-positive quarter. Behind it, a cohort of operators across six categories is reaching working economics at the same time.

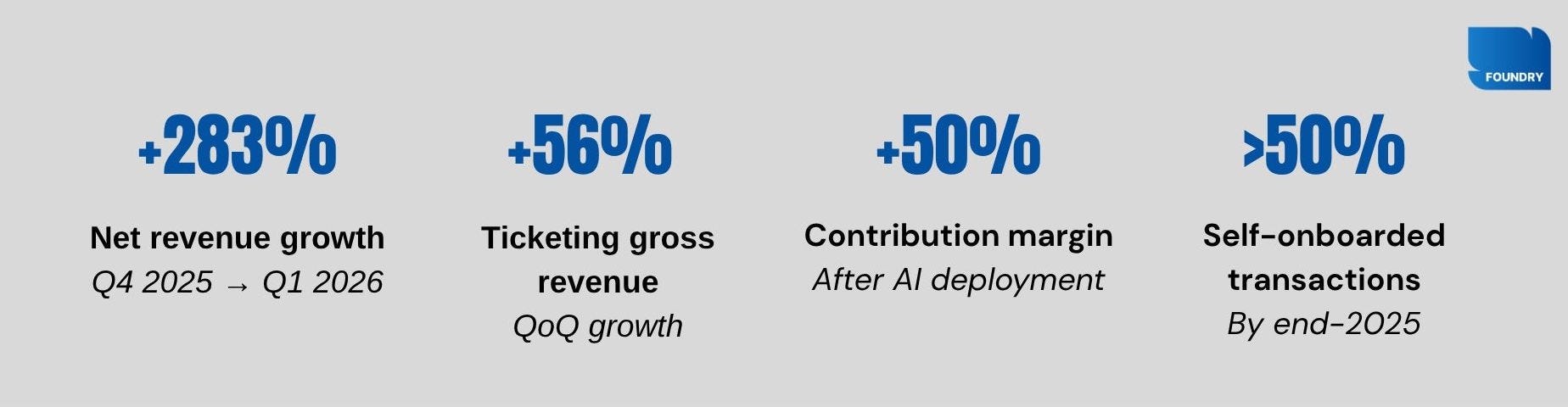

TipTip just closed Q1 2026 EBITDA positive, on the back of 283% net revenue growth and a 50% contribution margin expansion after AI deployment. Founder and CEO Albert Lucius spent five years rebuilding TipTip from a tipping tool into ticketing infrastructure for events and entertainment experiences, a category with structurally higher unit economics. The patience paid off. The result lands inside a market built for exactly this moment: a creative economy that contributed USD 100 billion to national GDP last year, supported 27.4 million jobs, and grew creative exports 67% in a single year. TipTip just proved that building a real business on top of that base is possible.

Behind TipTip, a cohort of operators across audio, OTT video, virtual influencer infrastructure, niche marketplaces, and music distribution are each reaching their own version of working economics, under different mechanisms, at different stages, in different cities. That breadth is what makes this moment different from any prior cycle.

TipTip: the pivot that compounded into a profit

From tipping tool to ticketing infrastructure, a multi-quarter repositioning that most of the market wasn’t watching

The EBITDA print TipTip delivered in Q1 2026 is the visible end of a repositioning that began well before this quarter. The platform that launched as a tipping and community-payments tool now operates as ticketing infrastructure for events and entertainment experiences, a category with structurally higher unit economics than tipping ever offered. Three things drove the result, and each one compounds the next.

Ticketing became the engine. Event ticketing charges organisers on gross transaction value, not on tip amounts — bigger denominator, higher margin per transaction, better operating leverage as volume scales.

AI compressed the cost of running it. TipTip’s demand-prediction system claims over 99% accuracy on ticket-sales forecasting, which means working-capital optimisation for event organisers is now a built-in feature, not an add-on service. Contribution margin grew after deployment. The cost that disappeared was the human underwriting layer that competitors still price for.

Self-serve supply removed the ceiling. By end-2025, more than half of all transactions came from promoters who onboarded themselves. Sales overhead at the marginal unit became effectively zero. The platform scales supply without scaling headcount.

The next leg is SatuSatu, a curated platform for cultural activities, outdoor tours, and workshops running on TipTip’s existing AI ticketing rails, plus a concierge layer combining automation with human support. CEO Albert Lucius framed the thesis in the May 2026 release: real-world experiences become more valuable as digital technologies evolve. SatuSatu is the bet that the fastest-growing GDP segment in Q1 2026 Accommodation and Food Services, up 13.14% is also the next inventory source for a ticketing platform already built to handle it.

The moat is in the demand-prediction data, built quietly while the playbook was being written.

The cohort: six categories, one industry

The more interesting story isn’t TipTip alone, it’s what the operators around it are building toward.

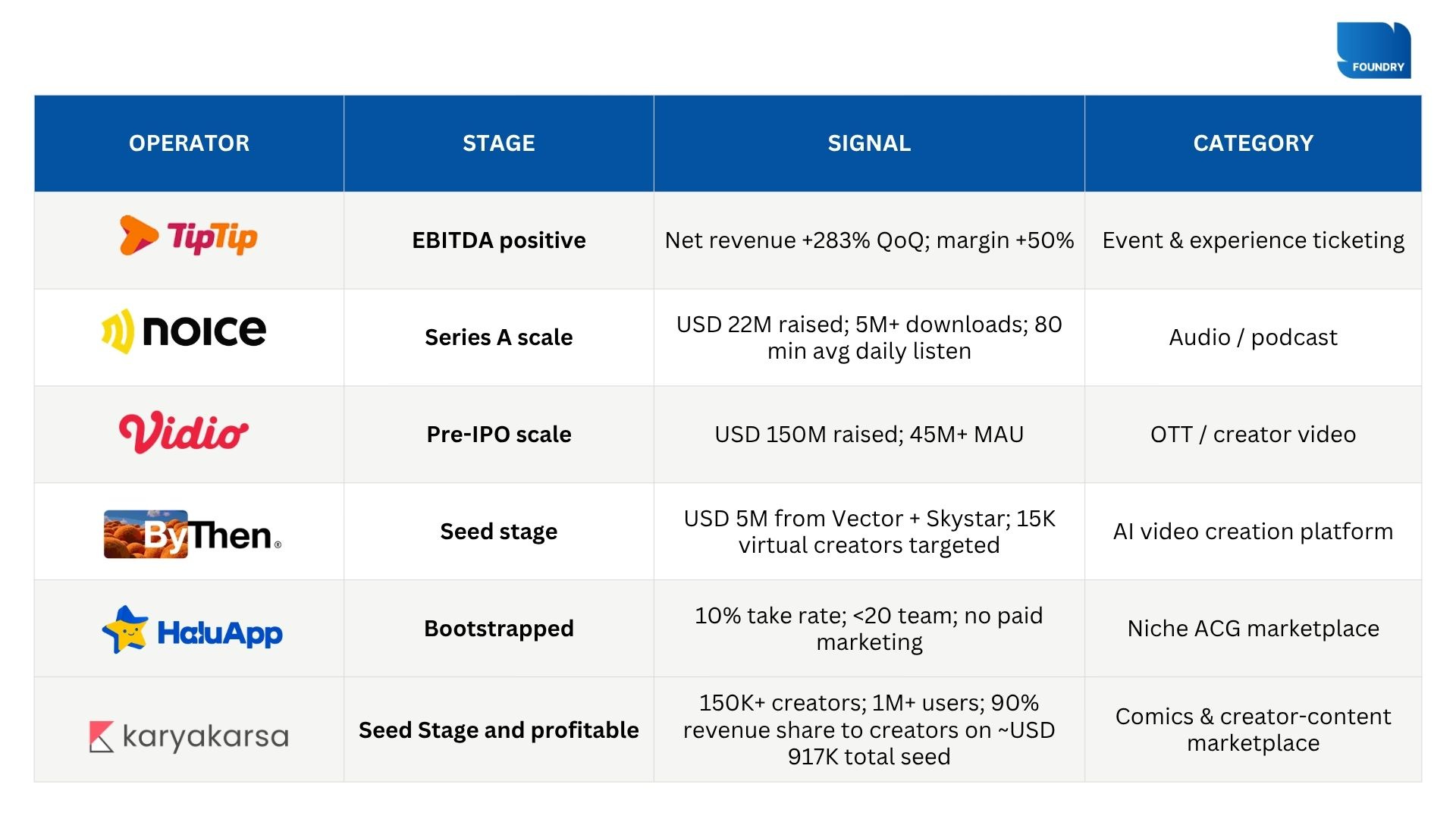

What this cohort has in common isn’t funding stage or category, it’s specificity. Each operator has identified a structural advantage narrow enough to defend: Noice in audio and podcasting, where Indonesia ranks second globally for weekly listeners. KaryaKarsa in story and comics with 150K+ creators. Vidio in premium OTT video, where 5M+ subscribers give the platform the scale to commission original content and run creator competitions simultaneously. Bythen in AI content creator video platform, where a founding team with two prior exits (Magnivate to WPP, Bridestory to Tokopedia) is building the picks-and-shovels layer for an influencer market that doesn’t yet need to show its face.

HaluApp is the most instructive case at the bottom of the table. Founded in 2022 in Surabaya, bootstrapped, fewer than 20 people, no paid digital marketing, and running a 10% take rate on a niche ACG marketplace that is cash-flow positive. The point isn’t that HaluApp will become the largest operator in the cohort.

The point is that category specificity plus operational discipline produces working economics at a fraction of the capital the first generation consumed.

The market gap the second generation is closing

The under-monetisation is real, which means so is the upside

Indonesia is currently a volume powerhouse, moving over IDR100 trillion (~USD6.198 billion) in transactions through sheer scale. The fact that per-transaction value still trails Singapore by 4x reveals a high-velocity opportunity for the next generation of digital operators. With a 39% annual growth rate and the region’s largest creator ecosystem, Indonesia is the ultimate frontier for those ready to turn massive digital engagement into premium economic val

The supporting infrastructure is already in place. Indonesia has 143 million social-media identities, 103 million Instagram users, and a digital ad market worth USD 6.45 billion in 2025. The creator economy market is projected to reach USD 112.7 billion by 2031 from USD 38.5 billion in 2025, a 19.7% CAGR, sitting inside a broader digital economy already near USD 100 billion in GMV. The audience-trust dynamics are structurally favourable: 67% of audiences report higher purchase intent from creators they perceive as genuine, and 86% reward consistency over reach.

What the second generation learned

The playbook changed. The results are following.

The first generation of Indonesia’s creator-economy platforms proved that demand was real. Creators wanted tools. Audiences were willing to pay. But the unit economics didn’t close at the scale those platforms reached, and most were absorbed, stalled, or remained subscale. That wasn’t a failure of the market. It was a failure of the model.

The second generation read the same market differently. Instead of building horizontal tipping or patronage tools for any creator, they went vertical — category-specific, geography-specific, or infrastructure-specific. TipTip went deep into live event ticketing and built AI underwriting on top of it. HaluApp went deep into ACG and built a community marketplace for a niche that mainstream platforms underserve. Bythen went upstream into the infrastructure layer that the next generation of virtual creators will run on.

The structural advantages compound in ways that horizontal platforms don’t. Pricing power holds in niches. AI capability reduces marginal cost. Geographic specificity keeps customer acquisition costs low. These aren’t incremental improvements on the first-generation playbook. They’re a different playbook.

TipTip’s EBITDA print is one data point in a much larger set. The set includes a bootstrapped marketplace in Surabaya running a 10% take rate with fewer than 20 people, an audio platform where Indonesians listen for 80 minutes a day, and an OTT platform with 45 million monthly users preparing for a public listing. These aren’t outliers. They’re the second generation and the question for the next twelve months isn’t whether the model works. It’s how broadly the pattern spreads.